In Example 3.6 use the WinBUGS jump RJMCMC interface to obtain the highest posterior probability model for

Question:

In Example 3.6 use the WinBUGS jump RJMCMC interface to obtain the highest posterior probability model for the Chevrolet asking price data, assuming a prior \(P_{\text {ret }} \sim\) \(\operatorname{Bin}(P, 0.5)\) on the number of retained predictors (with \(P=5\) ). This can be implemented by adapting the RJMCMC code from Example 3.3, including statements for the conjugate normal prior assumed in Example 3.6:

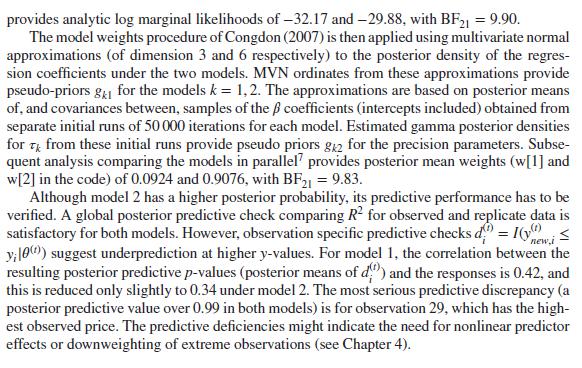

How far does this model remedy the predictive deficiencies identified in Example 3.6.

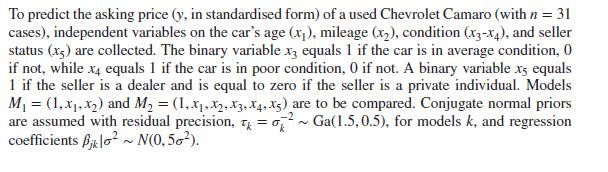

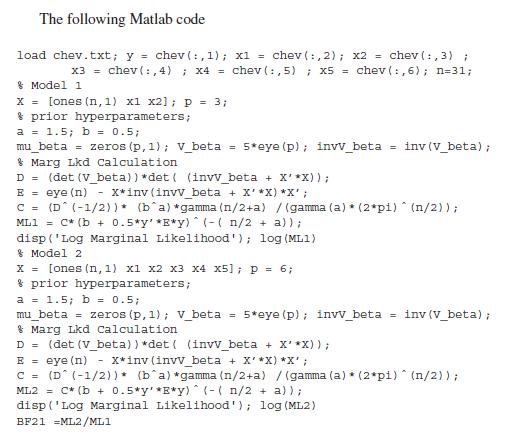

Data from Example 3.6

Fantastic news! We've Found the answer you've been seeking!

Step by Step Answer:

Answered By

Joseph Njoroge

I am a professional tutor with more than six years of experience. I have helped thousands of students to achieve their academic goals. My primary objectives as a tutor is to ensure that students do not have problems while tackling their academic problems.

10+ Reviews

27+ Question Solved

Related Book For

Question Posted: