Exercise 12.11 Consider a Brownian motion {X(t)} with drift and diffusion coefficient . Suppose that X(0)

Question:

Exercise 12.11 Consider a Brownian motion {X(t)} with drift μ and diffusion coefficient σ. Suppose that X(0) = 0, and let τ denote the first time that the Brownian motion reaches the state x > 0. Prove that the density function for τ is given by

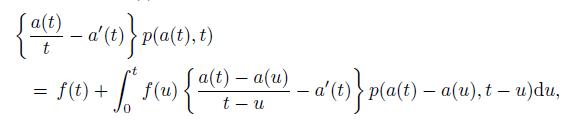

Note: For a standard Brownian motion {z(t)}, let τ be the first passage time to the boundary a(t) > 0. If the derivative a′(t) exists and is continuous, then the density function f(t) for τ satisfies the equation

where p(x, t) is the transition density function of {z(t)}. See Williams (1992)

for details.

Fantastic news! We've Found the answer you've been seeking!

Step by Step Answer:

Answered By

PALASH JHANWAR

I am a Chartered Accountant with AIR 45 in CA - IPCC. I am a Merit Holder ( B.Com ). The following is my educational details.

PLEASE ACCESS MY RESUME FROM THE FOLLOWING LINK: https://drive.google.com/file/d/1hYR1uch-ff6MRC_cDB07K6VqY9kQ3SFL/view?usp=sharing

3+ Reviews

10+ Question Solved

Related Book For

Stochastic Processes With Applications To Finance

ISBN: 9781439884829

2nd Edition

Authors: Masaaki Kijima

Question Posted: