a. Assume that the swap rate for an interest-rate swap is 7% and that the fixed-rate swap

Question:

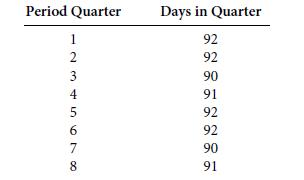

a. Assume that the swap rate for an interest-rate swap is 7% and that the fixed-rate swap payments are made quarterly on an actual/360 basis. If the notional amount of a two-year swap is $20 million, what is the fixed-rate payment at the end of each quarter assuming the following number of days in each quarter?

b. Assume that the swap in question a requires payments semiannually rather than quarterly.

What is the semiannual fixed-rate payment?

c. Suppose that the notional amount for the two-year swap is not the same in both years.

Suppose instead that in year 1 the notional amount is $20 million, but in year 2 the notional amount is $12 million. What is the fixed-rate payment every six months?

Fantastic news! We've Found the answer you've been seeking!

Step by Step Answer:

Answered By

OTIENO OBADO

I have a vast experience in teaching, mentoring and tutoring. I handle student concerns diligently and my academic background is undeniably aesthetic

3+ Reviews

10+ Question Solved

Related Book For

Question Posted: