Paul Wagtail started a small manufacturing business on 1 May 20X8. He has kept his records on

Question:

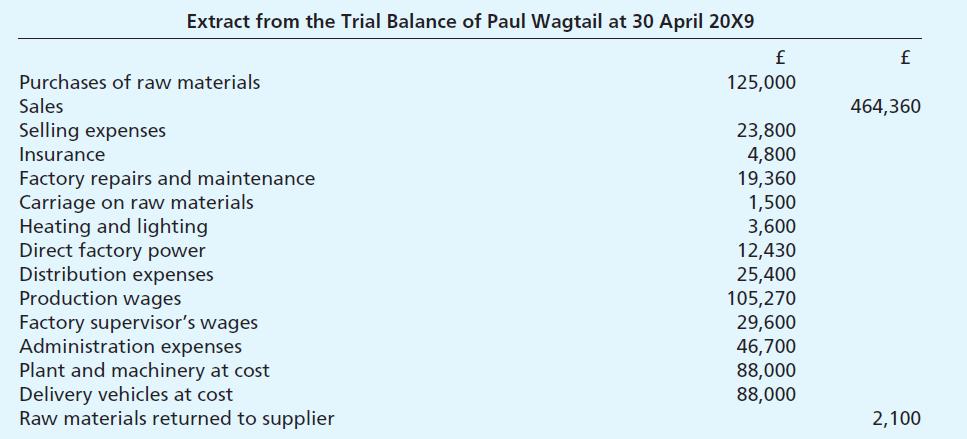

Paul Wagtail started a small manufacturing business on 1 May 20X8. He has kept his records on the double entry system, and has drawn up a trial balance at 30 April 20X9 before attempting to prepare his first final accounts.

At 30 April 20X9, he has closing stocks of raw materials costing £8,900. He has manufactured 9,500 completed units of his product, and sold 8,900. He has a further 625 units that are 80 per cent complete for raw materials and production labour, and also 80 per cent complete for factory indirect costs.

He has decided to divide his insurance costs and his heating and lighting costs 40 per cent for the factory and 60 per cent for the office/showroom.

He wishes to depreciate his plant and machinery at 20 per cent p.a. on cost, and his delivery vehicles using the reducing balance method at 40 per cent p.a.

He has not yet made up his mind how to value his stocks of work in progress and finished goods. He has heard that he could use either marginal or absorption costing to do this, and has received different advice from a friend running a similar business and from an accountant.

Required:

(a) Prepare Paul Wagtail’s manufacturing, trading and profit and loss accounts for the year ended 30 April 20X9 using both marginal and absorption costing methods, preferably in columnar format.

(b) Advise Paul Wagtail of the advantages and disadvantages of using each method.

Step by Step Answer:

a Manufacturing Trading and Profit Loss Accounts for the year ended 30 April 20X9 Marginal Costing Method Particulars Amount Sales 464360 Opening Stock of Finished Goods Add Cost of Production WIP 448...View the full answer

Frank Woods Business Accounting Volume 2

ISBN: 9780273693109

10th Edition

Authors: Frank Wood, Alan Sangster