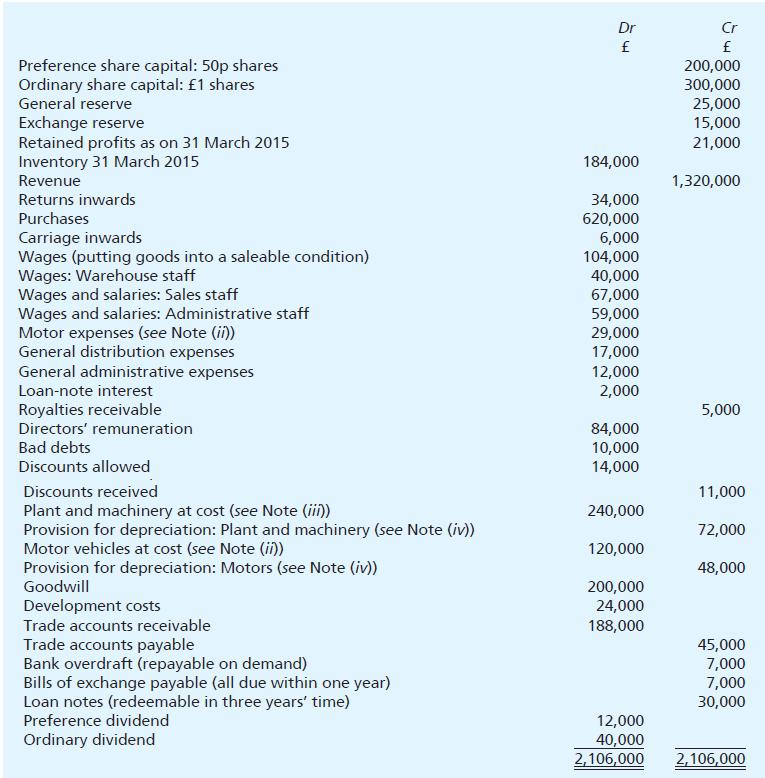

The trial balance of Jeremina plc as at 31 March 2016 is as follows: (i) Inventory of

Question:

The trial balance of Jeremina plc as at 31 March 2016 is as follows:

(i) Inventory of finished goods on 31 March 2016 £163,000.

(ii) Motor expenses and depreciation on motors to be apportioned: distribution 4/5, administrative 1/5.

(iii) Plant and machinery depreciation to be apportioned: cost of sales 7/10, distribution 1/5, administrative 1/10.

(iv) Depreciate the following non-current assets on cost: motor vehicles 20%, plant and machinery 15%.

(v) Accrue corporation tax on profits of the year £38,000. This is payable on 31 December 2016. You are to draw up:

(a) a detailed statement of profit or loss for the year ending 31 March 2016 for internal use, and

(b) a statement of profit or loss for publication, also a statement of financial position as at 31 March 2016.

Step by Step Answer:

Jeremina plc Statement of Profit or Loss for the Year Ending 31 March 2016 For Internal Use Particulars Amount Revenue 1320000 Cost of Goods Sold Open...View the full answer

Frank Woods Business Accounting Volume 2

ISBN: 9781292085050

13th Edition

Authors: Frank Wood, Alan Sangster