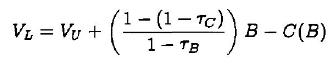

The general expression for the value of a leveraged firm in a world in which (tau_{S}=0) is

Question:

The general expression for the value of a leveraged firm in a world in which \(\tau_{S}=0\) is

where \(V_{U}\) is the value of an unlevered firm, \(\tau_{C}\) is the effective corporate tax rate for the firm, \(\tau_{B}\) is the personal tax rate of the marginal bondholder, \(B\) is the debt level of the firm, and \(C(B)\) is the present value of the costs of financial distress for the firm as a function of its debt level. (Note: \(C(B)\) encompasses all non-tax-related effects of leverage on the firm's value.)

Assume all investors are risk neutral.

1. In their no-tax model, what do Modigliani and Miller assume about \(\tau_{C}, \tau_{B}\) and \(C(B)\) ? What do these assumptions imply about a firm's optimal debt-equity ratio?

2. In their model that includes corporate taxes, what do Modigliani and Miller assume about \(\tau_{C}, \tau_{B}\) and \(C(B)\) ? What do these assumptions imply about a firm's optimal debt-equity ratio?

3. Assume that IBM is certain to be able to use its interest deductions to reduce its corporate tax bill. What would the change in the value of IBM be if the company issued \(\$ 1\) billion in debt and used the proceeds to repurchase equity? Assume that the personal tax rate on bond income is \(20 \%\), the corporate tax rate is \(34 \%\), and the costs of financial distress are zero.

Step by Step Answer:

Lectures On Corporate Finance

ISBN: 9789812568991

2nd Edition

Authors: Peter L Bossaerts, Bernt Arne Odegaard