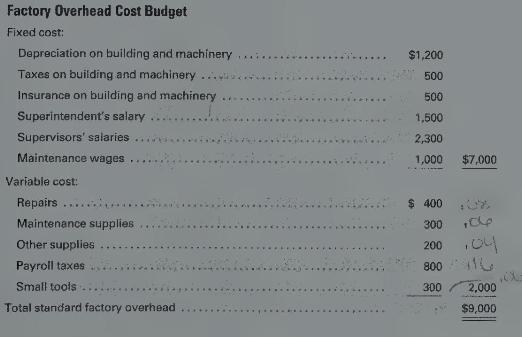

Flexible budget for factory overhead} Presented below are the monthly factory overhead cost budget (at normal capacity

Question:

Flexible budget for factory overhead}

Presented below are the monthly factory overhead cost budget (at normal capacity of 5,000 units or 20,000 direct labor hours) and the production and cost data for a month.

{Required:}

1. Assuming that variable costs will vary in direct proportion to the change in volume, prepare a flexible budget for production levels of \(80 \%, 90 \%\), and \(110 \%\) of normal capacity. Also determine the rate for application of factory overhead to work in process at each level of volume in both units and direct labor hours.

2. Prepare a flexible budget for production levels of \(80 \%, 90 \%\), and \(110 \%\), assuming that variable costs will vary in direct proportion to the change in volume, but with the following exceptions. (Hint: Set up a third category for semifixed expenses.)

a. At \(110 \%\) of capacity, an assistant department head will be needed at a salary of \(\$ 10,500\) annually.

b. At \(80 \%\) of capacity, the repairs expense will drop to one-half of the amount at \(100 \%\) capacity.

c. Maintenance supplies expense will remain constant at all levels of production.

d. At \(80 \%\) of capacity, one part-time maintenance worker, earning \(\$ 6,000\) a year, will be laid off.

e. At \(110 \%\) of capacity, a machine not normally in use and on which no depreciation is normally recorded will be used in production. Its cost was \(\$ 12,000\), it has a ten-year life, and straight-line depreciation will be taken.

3. Using the facts and the flexible budget prepared in 1., determine the budgeted cost at \(96 \%\) of capacity, using interpolation.

4. Using the flexible budget prepared in 1., determine the budgeted cost at \(104 \%\) of capacity, using a method other than interpolation.

Step by Step Answer: