Calculation of sales to achieve target profit and preparation of functional budgets There is a continuing demand

Question:

Calculation of sales to achieve target profit and preparation of functional budgets There is a continuing demand for three subassemblies

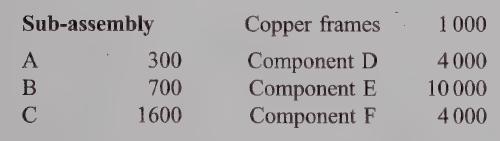

— A, B and C — made and sold by MW Limited. Sales are in the ratios of A 1, B 2, C 4 and selling prices are A £215, B £250, C £300. Each sub-assembly consists of a copper frame onto which are fixed the same components but in differing quantities as follows:

The skilled labour is paid £6 per hour and unskilled £4.50 per hour. The skilled labour is located in a machining department and the unskilled labour in an assembly department. A five-day week of 375 hours is worked and each accounting period is for four weeks.

Variable overhead per sub-assembly is A £5, B £4 and C £3.50. At the end of the current year, stocks are expected to be as shown below but because interest rates have increased and the company utilizes a bank overdraft for working capital purposes, it is planned to effect a 10%

reduction in all finished sub-assemblies and bought-in stocks during Period | of the forthcoming year.

Forecast stocks at current year end:

Work-in-progress stocks are to be ignored.

Overhead for the forthcoming year is budgeted to be Production £728 000, Selling and Distribution £364 000 and Administration £338 000. These costs, all fixed, are expected to be incurred evenly throughout the year and are treated as period costs.

Within Period | it is planned to sell one thirteenth of the annual requirements which are to be the sales necessary to achieve the company profit target of £6.5 million before tax.

You are required

(a) to prepare budgets in respect of Period 1 of the forthcoming year for (i) sales, in quantities and value;

(ii) production, in quantities only;

(iii) materials usage, in quantities;

(iv) materials purchases, in quantities and value;

(v) manpower budget, i.e. numbers of people needed in each of the machining department and the assembly department;

(20 marks)

(b) to discuss the factors to be considered if the bought-in stocks were to be reduced to one week’s requirements — this has been proposed by the purchasing officer but resisted by the production director.

Step by Step Answer: