Preparation of variable and absorption costing profit statements and comments in support of a variable costing system

Question:

Preparation of variable and absorption costing profit statements and comments in support of a variable costing system A manufacturer of glass bottles has been affected by competition from plastic bottles and is currently operating at between 65 and 70 per cent of maximum capacity.

The company at present reports profits on an absorption costing basis but with the high fixed costs associated with the glass container industry and a substantial difference between sales volumes and production in some months, the accountant has been criticized for reporting widely different profits from month to month. To counteract this criticism, he is proposing in future to report profits based on marginal costing and in his proposal to management lists the following reasons for wishing to change:

1. Marginal costing provides for the complete segregation of fixed costs, thus facilitating closer control of production costs.

2. It eliminates the distortion of interim profit statements which occur when there are seasonal fluctuations in sales volume although production is at a fairly constant level.

3. It results in cost information which is more helpful in determining the sales policy necessary to maximize profits.

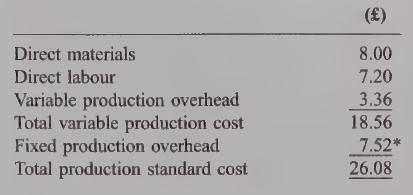

From the accounting records the following figures were extracted: Standard cost per gross (a gross is 144 bottles and is the cost unit used within the business):

*The fixed production overhead rate was based on the following computations:

Total annual fixed production overhead was budgeted at £7584 000 or £632 000 per month.

Production volume was set at 1008000 gross bottles or 70 per cent of maximum capacity.

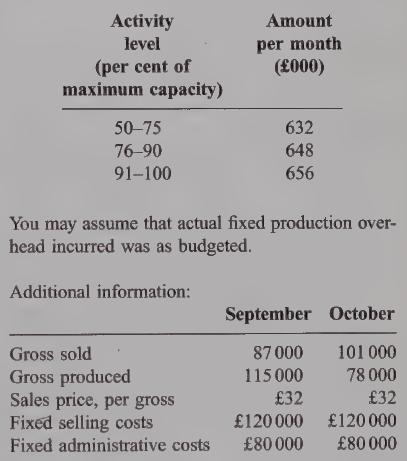

There is a slight difference in budgeted fixed production overhead at different levels of operating:

There were no finished goods in stock at 1 September.

You are required

(a) to prepare monthly profit statements for September and October using (i) absorption costing; and (ii) marginal costing; (16 marks)

(b) to comment briefly on the accountant’s three reasons which he listed to support his proposal.

Step by Step Answer: