A trader shorts one share of a stock index for 50 and buys a 60-strike European call

Question:

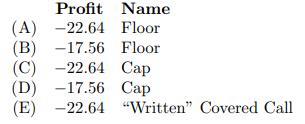

A trader shorts one share of a stock index for 50 and buys a 60-strike European call option on that stock that expires in 2 years for 10. Assume the annual effective risk-free interest rate is 3%. The stock index increases to 75 after 2 years. Calculate the profit on your combined position, and determine an alternative name for this combined position.

Fantastic news! We've Found the answer you've been seeking!

Step by Step Answer:

B A position consisting of a short asset position a...View the full answer

Answered By

Elias Gichuru

am devoted to my work and dedicated in helping my clients accomplish their goals and objectives,providing the best for all tasks assigned to me as a freelancer,providing high quality work that yields high scores.promise to serve them earnestly and help them achieve their goals.i have the needed expertise,knowledge and experience to handle their tasks.

325+ Reviews

859+ Question Solved

Related Book For

Question Posted: