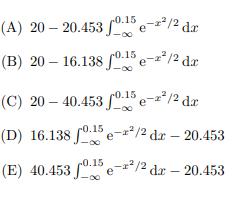

You are considering the purchase of a three-month 41.5-strike American call option on a nondividend-paying stock. You

Question:

You are considering the purchase of a three-month 41.5-strike American call option on a nondividend-paying stock.

You are given:

(i) The Black-Scholes framework holds.

(ii) The stock is currently selling for 40.

(iii) The stock’s volatility is 30%.

(iv) The current call option delta is 0.5.

Determine the current price of the option.

Fantastic news! We've Found the answer you've been seeking!

Step by Step Answer:

D It can be shown that it is never optimal to exer...View the full answer

Answered By

Rukhsar Ansari

I am professional Chartered accountant and hold Master degree in commerce. Number crunching is my favorite thing. I have teaching experience of various subjects both online and offline. I am online tutor on various online platform.

4+ Reviews

17+ Question Solved

Related Book For

Question Posted: