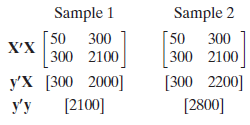

Two samples of 50 observations each produce the following moment matrices. (In each case, X is a

Question:

Two samples of 50 observations each produce the following moment matrices. (In each case, X is a constant and one variable.)

a. Compute the least squares regression coefficients and the residual variances s2 for each data set. Compute the R2 for each regression.

b. Compute the OLS estimate of the coefficient vector assuming that the coefficients and disturbance variance are the same in the two regressions. Also compute the estimate of the asymptotic covariance matrix of the estimate.

c. Test the hypothesis that the variances in the two regressions are the same without assuming that the coefficients are the same in the two regressions.

d. Compute the two-step FGLS estimator of the coefficients in the regressions, assuming that the constant and slope are the same in both regressions. Compute the estimate of the covariance matrix and compare it with the result of part b.

Step by Step Answer:

The sample moments are obtained using for example S xx x x n and so on For the two samples we obtain y x S xx S yy S xy Sample 1 6 6 300 300 200 Sampl...View the full answer