The cash flow measure that Ritter would most likely recommend to address Cannans concern is: A. free

Question:

The cash flow measure that Ritter would most likely recommend to address Cannan’s concern is:

A. free cash flow to equity.

B. earnings plus non-cash charges.

C. earnings before interest, tax, depreciation, and amortization.

Mark Cannan is updating research reports on two well-established consumer companies before first quarter 2011 earnings reports are released. His supervisor, Sharolyn Ritter, has asked Cannan to use market-based valuations when updating the reports.

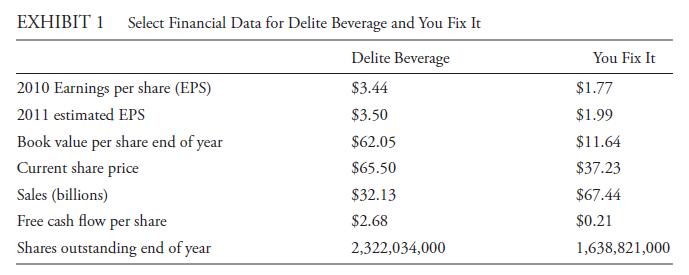

Delite Beverage is a manufacturer and distributor of soft drinks and recently acquired a major water bottling company in order to offer a broader product line. The acquisition will have a significant impact on Delite’s future results.

You Fix It is a United States retail distributor of products for home improvement, primarily for those consumers who choose to do the work themselves. The home improvement industry is cyclical; the industry was adversely affected by the recent downturn in the economy, the level of foreclosures, and slow home sales. Although sales and earnings at You Fix It weakened, same store sales are beginning to improve as consumers undertake more home improvement projects. Poor performing stores were closed, resulting in significant restructuring charges in 2010.

Before approving Cannan’s work, Ritter wants to discuss the calculations and choices of ratios used in the valuation of Delite and You Fix It. The data used by Cannan in his analysis is summarized in Exhibit 1.

Cannan advises Ritter that he is considering three different approaches to value the shares of You Fix It:

Approach 1: Price-to-book (P/B) ratio Approach 2: Price-to-earnings (P/E) ratio using trailing earnings Approach 3: Price-to-earnings ratio using normalized earnings Cannan tells Ritter that he calculated the price-to-sales ratio (P/S) for You Fix It, but chose not to use it in the valuation of the shares. Cannan states to Ritter that it is more appropriate to use the P/E ratio rather than the P/S ratio because:

Reason 1: Earnings are more stable than sales.

Reason 2: Earnings are less easily manipulated than sales.

Reason 3: The P/E ratio reflects financial leverage whereas the P/S ratio does not.

Cannan also informs Ritter that he did not use a price-to-cash flow multiple in valuing the shares of Delite or You Fix It. The reason is that he could not identify a cash flow measure that would both account for working capital and non-cash revenues, and also be after interest

Step by Step Answer: