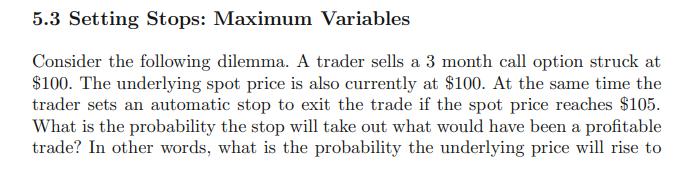

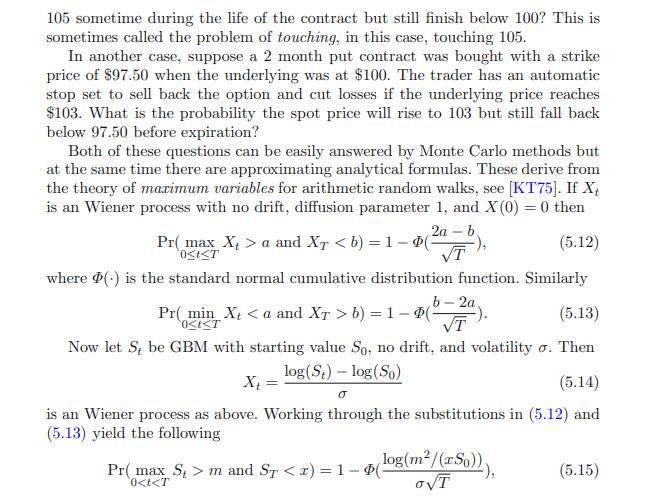

Answer the second dilemma in the section on maximum variables, Section 5.3. If the volatility is 20

Question:

Answer the second “dilemma” in the section on maximum variables, Section 5.3. If the volatility is 20 % and the time to expiration is 2 months, what is the probability that the stock price starting from 100 will rise above 103 over the term of theput option but nevertheless finish below 97.50? In the first case, assume the drift is zero. Write a program to answer the question if the drift is 6 %, if the drift is −4 %.

Data given in Section 5.3

Fantastic news! We've Found the answer you've been seeking!

Step by Step Answer:

To answer the second dilemma described in the section on maximum variables youll need to use the analytical formulas provided for the probability in a Geometric Brownian Motion GBM model with a drift ...View the full answer

Answered By

Khurram shahzad

I am an experienced tutor and have more than 7 years’ experience in the field of tutoring. My areas of expertise are Technology, statistics tasks I also tutor in Social Sciences, Humanities, Marketing, Project Management, Geology, Earth Sciences, Life Sciences, Computer Sciences, Physics, Psychology, Law Engineering, Media Studies, IR and many others.

I have been writing blogs, Tech news article, and listicles for American and UK based websites.

5+ Reviews

17+ Question Solved

Related Book For

Question Posted: