P6-75B. (Learning Objectives 1, 4: Estimating inventory by the gross profit method; preparing the Income Statement) Assume

Question:

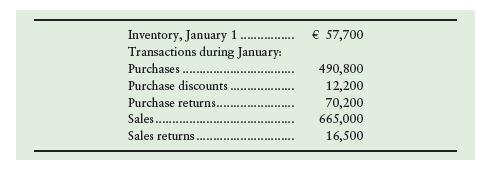

P6-75B. (Learning Objectives 1, 4: Estimating inventory by the gross profit method; preparing the Income Statement) Assume Joey Company, a sporting goods store, lost some inventory in a fire. To file an insurance claim, Joey Company must estimate its ending inventory by the gross profit method. Assume that for the past two years, Joey Company’s gross profit has averaged 45%

of net sales. Suppose Joey Company’s inventory records reveal the following data:

Requirements 1. Estimate the cost of the lost inventory, using the gross profit method.

2. Prepare the January Income Statement for this product through gross profit. Show the detailed computation of cost of goods sold in a separate schedule.

Step by Step Answer:

Financial Accounting International Financial Reporting Standards Global Edition

ISBN: 9781292211145

11th Edition

Authors: Charles T. Horngren, C. William Thomas, Wendy M. Tietz, Themin Suwardy, Walter T. Harrison