Mandatorily redeemable preferred shares substitute for debt and help manage the debt/equity ratio. (Adapted from an idea

Question:

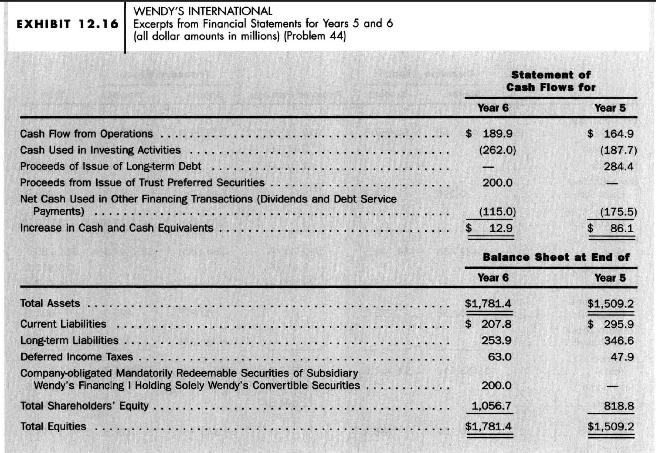

Mandatorily redeemable preferred shares substitute for debt and help manage the debt/equity ratio. (Adapted from an idea and materials provided by Katherine Schipper.) Exhibit 12.16 reproduces excerpts from the financial statements of Wendy's International for Years 5 and 6. The statement of cash flows indicates that Wendy's does not generate from operations sufficient cash to support its investing activities. In Year 5, Wendy's issued \(\$ 285\) million of long-term debt. It needed still more funds in Year 6, but did not want its balance sheet to show more debt.

It undertook the following series of transactions:

(1) Formed a subsidiary, Wendy's Financing I (Financing), wholly owned, to issue preferred equity and use the proceeds to acquire a single asset, bonds issued by Wendy's, (2) Caused the subsidiary to issue to the public \(\$ 200\) million of preferred shares which Wendy's guaranteed just as though it were Wendy's debt issue, and (3) Issued \(\$ 202\) million of its own debt to Financing in return for the cash Financing had just raised from the preferred issue.

After this series of transactions, the public holds preferred shares with Wendy's guarantee, which means that the market will price those shares much as it would Wendy's debt with similar guarantees. Wendy's describes the results of this series of transactions as follows, taken from its notes:

\section*{Note 3. Company-Obligated Mandatorily Redeemable Preferred Securities}

In September, Year 6, Wendy's Financing I (the trust) issued \(\$ 200,000,000\) of \(\$ 2.50\) Term Convertible Securities, Series A (the trust preferred securities). Wendy's Financing \(\mathrm{I}\), a statutory business trust, is a wholly-owned consolidated subsidiary of the company with its sole asset being \(\$ 202\) million aggregate principal amount of \(5 \%\) Convertible Subordinated Debentures due September 15, Year 26, of Wendy's (the trust debenture).

The trust preferred securities are non-voting (except in limited circumstances), pay quarterly distributions at an annual rate of \(5 \%\), carry a liquidation value of \(\$ 50\) per share and are convertible into the company's common shares at any time prior to the close of business on September 15, Year 26, at the option of the holder. The trust preferred securities are convertible into common shares. . . . The company [that is, Wendy's] has executed a guarantee with regard to the trust preferred securities. The guarantee, when taken together with the company's obligations under the trust indenture, the indenture pursuant to which the trust indenture was issued, and the applicable trust document, provides a full and an unconditional guarantee of the trust's obligations under the trust preferred securities.

In thinking about and responding to the questions below, you may ignore income taxes. Firms pay careful attention to the income tax treatment of securities such as the ones in this case, but you do not need to worry about such issues here.

a. Explain why Wendy's might prefer this series of transactions to one where it directly issued its debt in the market.

b. Why does the debt issued by Wendy's not appear on Wendy's balance sheet?

c. Compute Wendy's debt/equity ratio for the end of Year 5 and Year 6. For Year 6, make two calculations, one assuming the mandatorily preferred is debt and the other, assuming it is shareholders' equity. Treat Deferred Income Taxes as Shareholders' Equity in all calculations.

Step by Step Answer:

Financial Accounting An Introduction To Concepts Methods And Uses

ISBN: 9780324183511

10th Edition

Authors: Clyde P. Stickney, Roman L. Weil