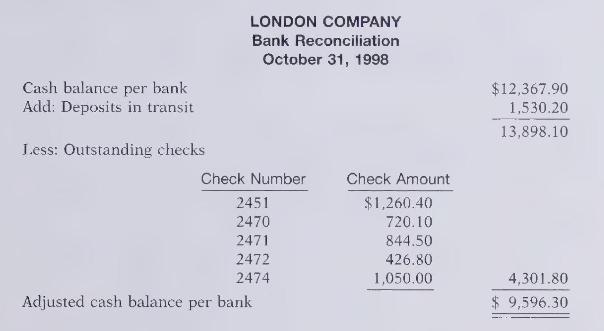

The bank portion of the bank reconciliation for London Company at October 31, 1998, is shown here:

Question:

The bank portion of the bank reconciliation for London Company at October 31, 1998, is shown here:

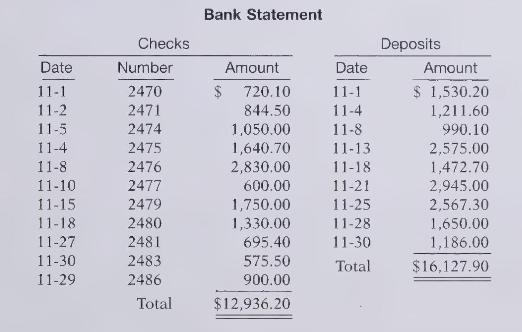

The adjusted cash balance per bank agreed with the cash balance per books at October 31. The November bank statement showed the following checks and deposits:

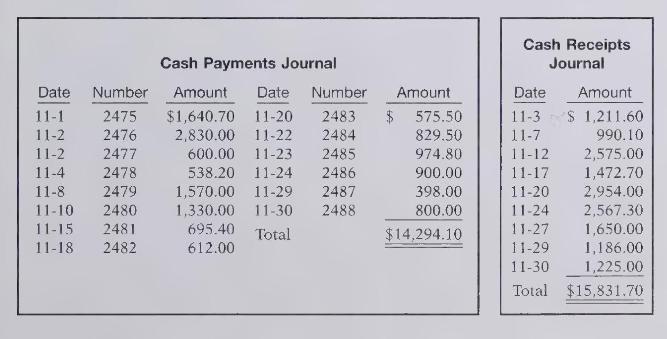

The cash records per books for November showed the following:

The bank statement contained two bank memoranda:

1. A credit of \(\$ 2,105.00\) for the collection of a \(\$ 2,000\) note for London Company plus interest of \(\$ 120\) and less a collection fee of \(\$ 15\). London Company has not accrued any interest on the note.

2. A debit for the printing of additional company checks \(\$ 50.00\).

At November 30 the cash balance per books was \(\$ 11,133.90\) and the cash balance per bank statement was \(\$ 17,614.60\). The bank did not make any errors, but two errors were made by London Company.

\section*{Instructions}

(a) Using the four steps in the reconciliation procedure described on pages 300-301, prepare a bank reconciliation at November 30 .

(b) Prepare the adjusting entries based on the reconciliation. [Note: The correction of any errors pertaining to recording checks should be made to Accounts Payable. The correction of any errors relating to recording cash receipts should be made to Accounts Receivable.]

Step by Step Answer:

Financial Accounting Tools For Business Decision Making

ISBN: 9780471169192

1st Edition

Authors: Paul D. Kimmel, Jerry J. Weygandt, Donald E. Kieso