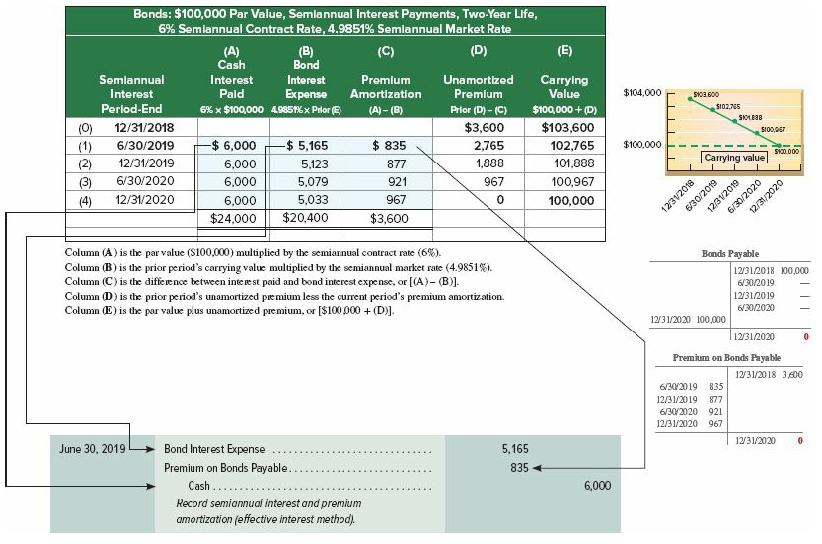

Refer to the bond details in Problem 10-4A. Ellis Company issues 6.5%, five-year bonds dated January 1,

Question:

Refer to the bond details in Problem 10-4A.

Ellis Company issues 6.5%, five-year bonds dated January 1, 2018, with a $250,000 par value. The bonds pay interest on June 30 and December 31 and are issued at a price of $255,333. The annual market rate is 6% on the issue date.

Required

1. Compute the total bond interest expense over the bonds? life.

2. Prepare an effective interest amortization table like the one in Exhibit 10B.2 for the bonds? life.

3. Prepare the journal entries to record the first two interest payments.

4. Use the market rate at issuance to compute the present value of the remaining cash flows for these bonds as of December 31, 2020. Compare your answer with the amount shown on the amortization table as the balance for that date (from part 2) and explain your findings.

Step by Step Answer:

Part 1 Ten payments of 8125 81250 Par value at maturity 250000 Total repaid 331250 Less amount borro...View the full answer

Financial Accounting Information for Decisions

ISBN: 978-1259917042

9th edition

Authors: John J. Wild