Derive a formula for the weights of the minimum variance portfolio of two stocks using the following

Question:

Derive a formula for the weights of the minimum variance portfolio of two stocks using the following steps:

a. Compute the variance of a portfolio with weights x and 1 - x on stocks 1 and 2, respectively.

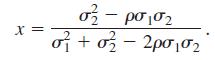

Show that you get![]()

b. Take the derivative with respect to x of the expression in part

a. Show that the value of x that makes the derivative 0 is

c. Compute the covariance of the return of this minimum variance portfolio with stocks 1 and 2.AppendixLO1

Fantastic news! We've Found the answer you've been seeking!

Step by Step Answer:

Answered By

Emily Grace

With over a decade of experience providing top-notch study assistance to students globally, I am dedicated to ensuring their academic success. My passion is to deliver original, high-quality assignments with fast turnaround times, always striving to exceed their expectations.

3+ Reviews

24+ Question Solved

Related Book For

Financial Markets And Corporate Strategy

ISBN: 9780077119027

1st Edition

Authors: David Hillier, Mark Grinblatt, Sheridan Titman

Question Posted: