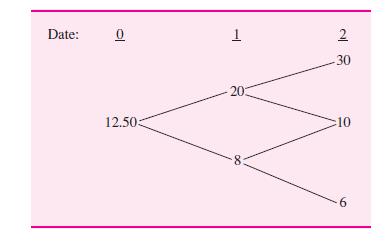

8.15. The following tree diagram outlines the price of a stock over the next two periods: The...

Question:

8.15. The following tree diagram outlines the price of a stock over the next two periods:

The risk-free rate is 12 percent from date 0 to date 1 and 15 percent from date 1 to date 2. A European call on this stock (1) expires in period 2 and (2) has a strike price of $8.

(a) Calculate the risk-neutral probabilities implied by the binomial tree.

(b) Calculate the payoffs of the call option at each of three nodes at date 2.

(c) Compute the value of the call at date 0.

Fantastic news! We've Found the answer you've been seeking!

Step by Step Answer:

Answered By

Lilian Nyambura

Hi, am Lilian Nyambura, With extensive experience in the writing industry, I am the best fit for your writing projects. I am currently pursuing a B.A. in Business Administration. With over 5 years of experience, I can comfortably say I am good in article writing, editing and proofreading, academic writing, resumes and cover letters. I have good command over English grammar, English Basic Skills, English Spelling, English Vocabulary, U.S. English Sentence Structure, U.K. or U.S. English Punctuation and other grammar related topics. Let me help you with all your essays, assignments, projects, dissertations, online exams and other related tasks. Quality is my goal.

378+ Reviews

750+ Question Solved

Related Book For

Financial Markets And Corporate Strategy

ISBN: 9780071157612

2nd Edition

Authors: Mark Grinblatt, Sheridan Titman

Question Posted: