Consider a European-style option on a non-dividend-paying stock share, whose price follows a geometric Brownian motion with

Question:

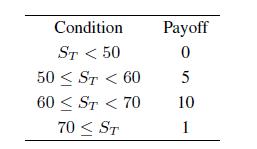

Consider a European-style option on a non-dividend-paying stock share, whose price follows a geometric Brownian motion with drift 5% and volatility 35% (per year); the continuously compounded risk-free rate is 3%; the option matures in 4 months, and the current underlying asset price is \($50.\) The payoff (in USD) is given by the following contingency table depending on the terminal price of the underlying asset:

Find the option price.

Fantastic news! We've Found the answer you've been seeking!

Step by Step Answer:

Answered By

Muhammad Rehan

Enjoy testing and can find bugs easily and help improve the product quality.

10+ Reviews

10+ Question Solved

Related Book For

An Introduction To Financial Markets A Quantitative Approach

ISBN: 9781118014776

1st Edition

Authors: Paolo Brandimarte

Question Posted: