Heres a simplified version of exercise 10. Consider an alternative parameterization of the binomial: Construct binomial European

Question:

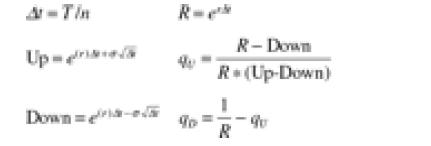

Here’s a simplified version of exercise 10.

Consider an alternative parameterization of the binomial:

Construct binomial European call and put option pricing functions in VBA for this parameterization and show that they also converge to the Black-Scholes formula. (The message here is that the parameterization of the binomial Up and Down is not unique.)

Fantastic news! We've Found the answer you've been seeking!

Step by Step Answer:

Answered By

Ashish Jaiswal

I have completed B.Sc in mathematics and Master in Computer Science.

20+ Reviews

39+ Question Solved

Related Book For

Question Posted: