In a well-known paper, Roll (1978), discusses tests of the SML in a four-asset context: a. Derive

Question:

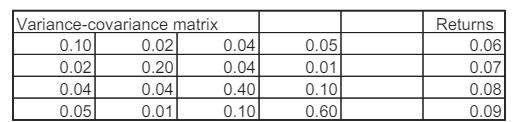

In a well-known paper, Roll (1978), discusses tests of the SML in a four-asset context:

a. Derive two effi cient portfolios in this four-asset model and draw a graph of the effi cient frontier.

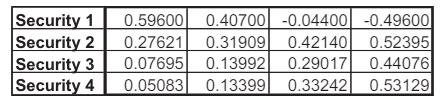

b. Show that the following four portfolios are effi cient by proving that each is a convex combination of the two portfolios you derived in part a:

c. Suppose that the market portfolio is composed of equal proportions of each asset (i.e., the market portfolio has proportions [0.25, 0.25, 0.25, 0.25]). Calculate the resulting SML. Is the portfolio [0.25, 0.25, 0.25, 0.25] effi cient?

d. Repeat this exercise, but substitute one of the four portfolios from part b as the candidate for the market portfolio.

Step by Step Answer:

This question has not been answered yet.

You can Ask your question!

Related Book For

Question Posted: