The following information is based on an actual annual report. Different names and years are being used.

Question:

The following information is based on an actual annual report. Different names and years are being used.

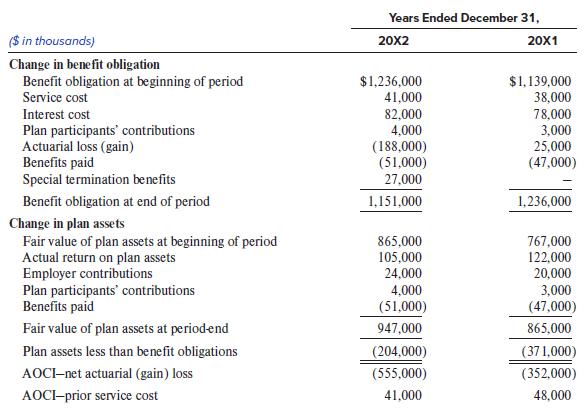

Bond and some of its subsidiaries provide certain postretirement medical, dental, and vision care and life insurance for retirees and their dependents and for the surviving dependents of eligible employees and retirees. Generally, the employees become eligible for postretirement benefits if they retire no earlier than age 55 with 10 years of service. The liability for postretirement benefits is funded through trust funds based on actuarially determined contributions that consider the amount deductible for income tax purposes. The health care plans are contributory, funded jointly by the companies and the participating retirees. The December 31, 20X2 and 20X1, postretirement benefit liabilities and related data were determined using the January 1, 20X2, actuarial valuations.

Information related to the accumulated postretirement benefit obligation plan for the years 20X2 and 20X1 follows:

The assumed discount rates used to determine the benefit obligation as of December 31, 20X2 and 20X1, were 7.75% and 6.75%, respectively. The fair value of plan assets excludes $9 million and $7 million held in a grantor trust as of December 31, 20X2 and 20X1, respectively, for the payment of postretirement medical benefits.

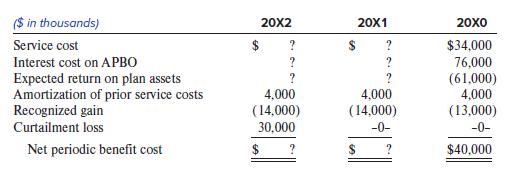

The components of other postretirement benefit costs, portions of which were recorded as components of construction costs for the years 20X2, 20X1, and 20X0, follow:

The other postretirement benefit curtailment losses in December 20X2 represent the recognition of $3,000 of additional prior service costs and a $27,000 increase in the benefit obligations resulting from special termination benefits.

The health care cost trend rates used to measure the expected cost of the postretirement medical benefits are assumed to be 8.0% for pre-Medicare recipients and 6.0% for Medicare recipients for 20X2. Those rates are assumed to decrease in 0.5% annual increments to 5% for the years 20X5 and 20X4, respectively, and to remain level thereafter. The health care cost trend rates, used to measure the expected cost of postretirement dental and vision benefits, are a level 3.5% and 2.0% per year, respectively. Assumed health care cost trend rates have a significant effect on the amounts reported for the health care plans.

Required:

1. Assuming an expected rate of return on plan assets for 20X2 and 20X1 of 8.8% and 9%, respectively, compute the missing amounts in the first table and determine the Net periodic benefit cost for years 20X2 and 20X1. (Round amounts to nearest million.)

2. Assuming that the employer submitted the $4,000,000 of participant contributions directly to the trust, show the journal entry that Bond would make to record its 20X2 company (employer) contribution, Net periodic benefit cost, and AOCI effects.

3. Show that the 20X2 journal entries result in a balance sheet pension asset (liability) equal to the funded status. Assume that the beginning 20X2 balance equals the ending 20X1 funded status.

Step by Step Answer:

Requirement 1 Determining missing costs and net periodic benefit cost 20X2 20X1 Service cost per cha...View the full answer

Financial Reporting And Analysis

ISBN: 9781260247848

8th Edition

Authors: Lawrence Revsine, Daniel Collins, Bruce Johnson, Fred Mittelstaedt, Leonard Soffer