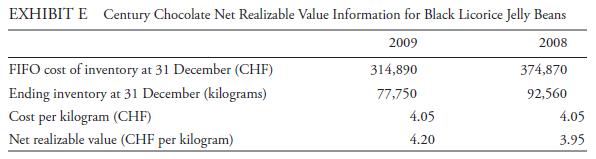

Using the inventory record for purchased lemon drops shown in Exhibit D, the cost of sales for

Question:

Using the inventory record for purchased lemon drops shown in Exhibit D, the cost of sales for 2009 will be closest to:

A. CHF 3,550.

B. CHF 4,550.

C. CHF 4,850.

Hans Annan, CFA, a food and beverage analyst, is reviewing Century Chocolate’s inventory policies as part of his evaluation of the company. Century Chocolate, based in Switzerland, manufactures chocolate products and purchases and resells other confectionery products to complement its chocolate line. Annan visited Century Chocolate’s manufacturing facility last year. He learned that cacao beans, imported from Brazil, represent the most significant raw material and that the work-in-progress inventory consists primarily of three items: roasted cacao beans, a thick paste produced from the beans (called chocolate liquor), and a sweetened mixture that needs to be “conched” to produce chocolate. On the tour, Annan learned that the conching process ranges from a few hours for lower-quality products to six days for the highest-quality chocolates. While there, Annan saw the facility’s climate-controlled area where manufactured finished products (cocoa and chocolate) and purchased finished goods are stored prior to shipment to customers. After touring the facility, Annan had a discussion with Century Chocolate’s CFO regarding the types of costs that were included in each inventory category.

Annan has asked his assistant, Joanna Kern, to gather some preliminary information regarding Century Chocolate’s financial statements and inventories. He also asked Kern to calculate the inventory turnover ratios for Century Chocolate and another chocolate manufacturer for the most recent five years. Annan does not know Century Chocolate’s most direct competitor, so he asks Kern to do some research and select the most appropriate company for the ratio comparison.

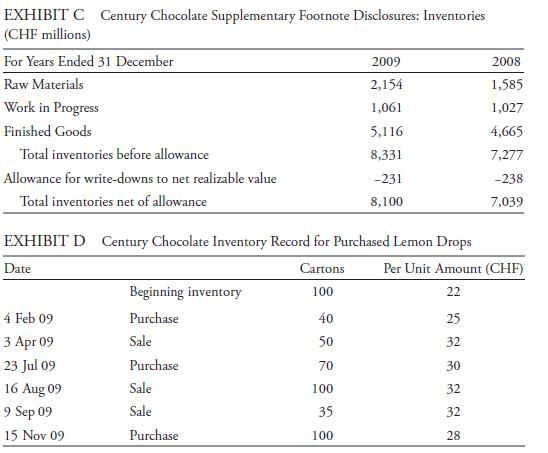

Kern reports back that Century Chocolate prepares its financial statements in accordance with IFRS. She tells Annan that the policy footnote states that raw materials and purchased finished goods are valued at purchase cost whereas work in progress and manufactured finished goods are valued at production cost. Raw material inventories and purchased finished goods are accounted for using the FIFO (first-in, first-out) method, and the weighted average cost method is used for other inventories. An allowance is established when the net realizable value of any inventory item is lower than the value calculated.

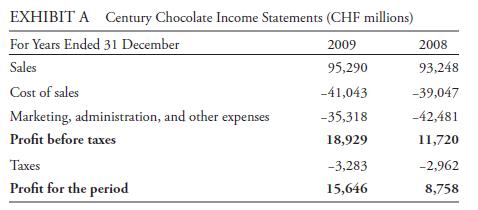

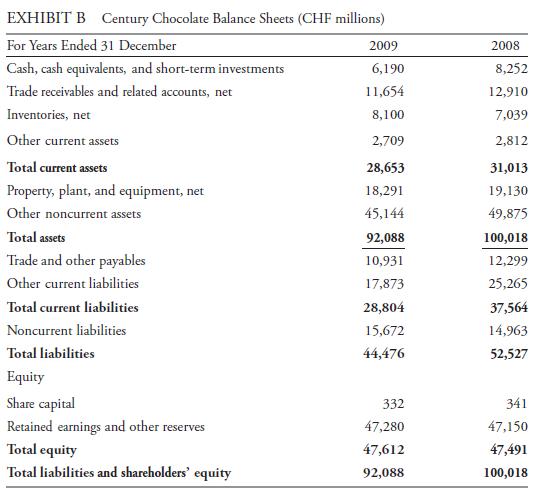

Kern provides Annan with the selected financial statements and inventory data for Century Chocolate shown in Exhibits A through E. The ratio exhibit Kern prepared compares Century Chocolate’s inventory turnover ratios to those of Gordon’s Goodies, a U.S.-based company. Annan returns the exhibit and tells Kern to select a different competitor that reports using IFRS rather than U.S. GAAP. During this initial review, Annan asks Kern why she has not indicated whether Century Chocolate uses a perpetual or a periodic inventory system. Kern replies that she learned that Century Chocolate uses a perpetual system but did not include this information in her report because inventory values would be the same under either a perpetual or periodic inventory system. Annan tells Kern she is wrong and directs her to research the matter.

While Kern is revising her analysis, Annan reviews the most recent month’s Cocoa Market Review from the International Cocoa Organization. He is drawn to the statement that “the ICCO daily price, averaging prices in both futures markets, reached a 29-year high in US$

terms and a 23-year high in SDRs terms (the SDR unit comprises a basket of major currencies used in international trade: US$, Euro, Pound Sterling, and Yen).” Annan makes a note that he will need to factor the potential continuation of this trend into his analysis.

Step by Step Answer:

Based on the information provided in Exhibit D the cost of sales for 2009 will be closest to CHF 455...View the full answer

International Financial Statement Analysis CFA Institute Investment Series

ISBN: 9780470287668

1st Edition

Authors: Thomas R. Robinson, Hennie Van Greuning CFA, Elaine Henry, Michael A. Broihahn, Sir David Tweedie