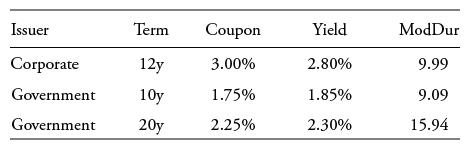

An active portfolio manager observes the following market information related to an outstanding corporate bond and two

Question:

An active portfolio manager observes the following market information related to an outstanding corporate bond and two on-the-run government bonds that pay annual coupons:

The portfolio manager also observes 10-year and 20-year swap spreads of 0.20% and 0.25%, respectively.

Calculate the I-spread of the corporate bond.

A. 0.85%

B. 0.65%

C. 0.95%

Fantastic news! We've Found the answer you've been seeking!

Step by Step Answer:

Answered By

Priya Mishra

Hi, I am Priya Mishra. I am a graduate in science subject. I love tutoring and I have started tutoring as soon as I had completed my schooling. I have started tutoring on online platforms as well such as on chegg, Bartleby and Fellow expert. I think I know the need of a student because I have also been a student before. I make sure that my students didn't feel less in terms of their learning and understanding experience. I am very good at describing and making students understand the concept behind the question. I never leave my students halfway in their learning journey.

0 Reviews

10+ Question Solved

Related Book For

Question Posted: