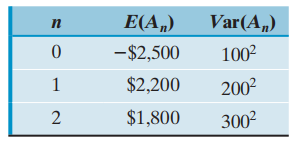

Consider an investment with the following projected cash flows: The distributions are assumed to be independent of

Question:

The distributions are assumed to be independent of each other.

(a) Compute the mean of the NPW at i = 10%. Using just the mean value, would the investment be accepted?

(b) Compute the standard deviation of the NPW distribution.

(c) Compute the two standard deviations below the mean. If these cash flows are normally distributed with the means and variances as previously specified, what is the probability that the actual NPW will fall 2σ below the mean?

Fantastic news! We've Found the answer you've been seeking!

Step by Step Answer:

a b c Using Excel ...View the full answer

Answered By

PRIYA KHURANA

My education details;

I have my graduation from Delhi University with 91.68%

I have my post graduation in MSc applied Chemistry with 8.91 CGPA.

I always maintain my academic records.

I have five years of tutoring experience as home tutor and in Chemistry coaching institutes and I worked up on variety of subjects. I have good subjective command in Chemistry and Physics. From my past teaching experience I have gained excellent knowledge in presenting the content to the students and enable them to understand all concepts.

I used to work part time as subject matter expert also from past four years for chemistry, maths and chemical engineering subjects.

Thus, I wish to contribute my knowledge and experience obtained so far in helping and assisting students in their projects as I believe I am having that inherent capability.

I believe in giving my hundred percent contribution in each and every work.

I will guide you the right path of success.

Thanks

0 Reviews

10+ Question Solved

Related Book For

Question Posted: