Costco expects payment for merchandise at the time of sale. The company accepts cash, checks, debit cards,

Question:

Costco expects payment for merchandise at the time of sale. The company accepts cash, checks, debit cards, and credit cards. These transactions do not result in an accounts receivable balance. Even so, the company's balance sheet does report an amount for accounts receivable.

Instructions:

Using Appendix B on page B-11 in this textbook, refer to Costco's Notes to Consolidated Financial Statements to answer the following questions.

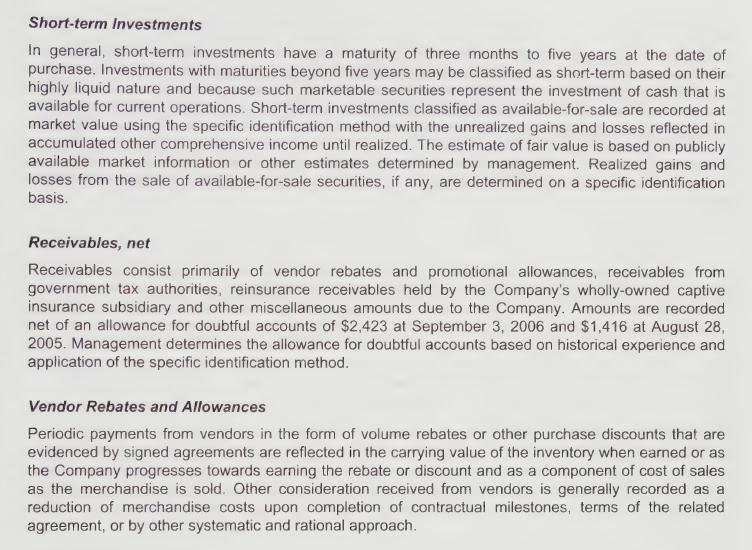

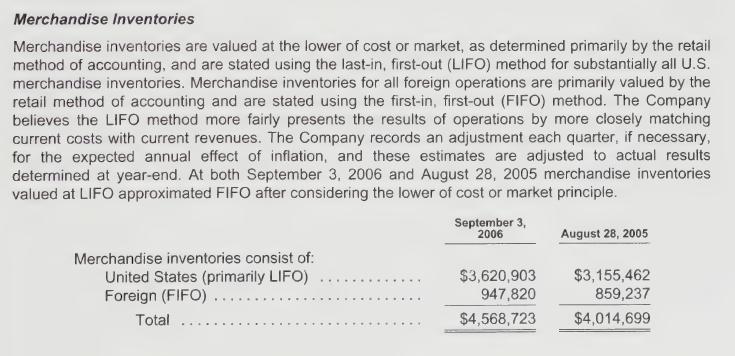

1. What is the content of net receivables?

2. What are the amounts for allowance for doubtful accounts on August 28, 2005 and September 3, 2006?

3. How do you think the allowance for doubtful accounts would change if Costco granted credit to its customers?

Data from Appendix B on page B-11

Fantastic news! We've Found the answer you've been seeking!

Step by Step Answer:

Answered By

Saleem Abbas

Have worked in academic writing for an a years as my part-time job.

1+ Reviews

10+ Question Solved

Related Book For

Question Posted: