Marshalls Devices uses activity-based costing to allocate overhead costs to customer orders for pricing purposes. Many customer

Question:

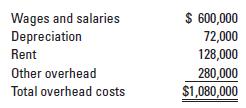

Marshall’s Devices uses activity-based costing to allocate overhead costs to customer orders for pricing purposes. Many customer orders are won through competitive bidding. Direct material and direct manufacturing labor costs are traced directly to each order. Marshall’s Devices direct manufacturing labor rate is $25 per hour. The company reports the following yearly overhead costs:

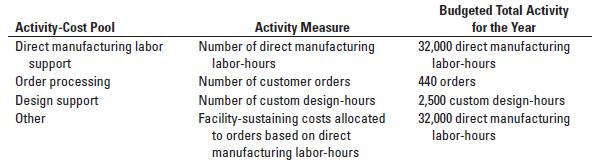

Marshall’s Devices has established four activity cost pools:

Some customer orders require more complex designs, while others need simple designs. Marshall estimates that it will do 100 complex designs during a year, which will each take 13 hours for a total of 1,300 design-hours. It estimates it will do 150 simple designs, which will each take 8 hours for a total of 1,200 design-hours.

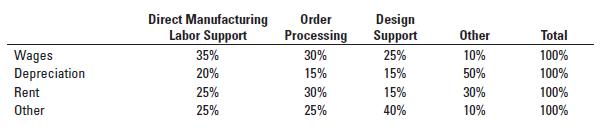

Paul Napoli, Marshall’s Devices’ controller, has prepared the following estimates for distribution of the overhead costs across the four activity cost pools:

Order 277100 consists of six different metal products. Four products require a complex design and two require a simple design. Order 277100 requires $5,500 of direct materials and 100 direct manufacturing labor-hours.

Required

1. Allocate the overhead costs to each activity cost pool. Calculate the activity rate for each pool.

2. Determine the cost of Order 277100.

3. How does activity-based costing enhance Marshall’s Devices’ ability to price its orders? Suppose Marshall’s Devices used a traditional costing system to allocate all overhead costs to orders on the basis of direct manufacturing labor-hours. How might this have affected Marshall’s Devices’ pricing decisions?

4. When designing its activity-based costing system, Marshall uses time-driven activity-based costing (TDABC) system for its design department. What does this approach allow Marshall to do? How would the cost of Order 277100 have been different if Marshall has used the number of customer designs rather than the number of custom design-hours to allocate costs to different customer orders? Which cost driver do you prefer for design support? Why?

Step by Step Answer:

Allocation of overhead costs to each activity cost pool and calculation of activity rate for each pool ActivityCost Pool Wages Depreciation Rent Other ...View the full answer

Horngrens Cost Accounting A Managerial Emphasis

ISBN: 9780135628478

17th Edition

Authors: Srikant M. Datar, Madhav V. Rajan