Sharma Corporation has decided that, in preparing its 2020 financial statements under IFRS, two changes should be

Question:

Sharma Corporation has decided that, in preparing its 2020 financial statements under IFRS, two changes should be made from the methods used in prior years:

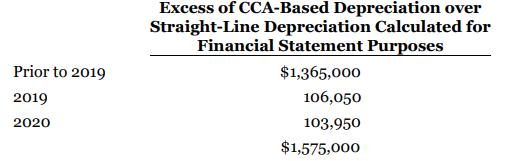

1. Depreciation. Sharma has used the tax basis (CCA) method of calculating depreciation for financial reporting purposes. During 2020, management decided that the straight-line method should have been used to calculate depreciation for financial reporting purposes for the years prior to 2020 and going forward. The following schedule identifies the excess of depreciation based on CCA over depreciation based on straightline, for the past years and for the current year:

Depreciation is charged 75% to cost of sales and 25% to selling, general, and administrative expenses.

2. Bad debt expense. In the past, Sharma recognized bad debt expense equal to 1.5% of net sales. After careful review, it has been decided that a rate of 1.75% is more appropriate for 2020. Bad debt expense is charged to selling, general, and administrative expenses.

The following information is taken from preliminary financial statements, which were prepared before including the effects of the two changes.

Step by Step Answer:

The two changes in Sharma Corporation s 2020 financial statements under IF RS would affect the follo...View the full answer

Intermediate Accounting Volume 2

ISBN: 9781119497042

12th Canadian Edition

Authors: Donald E. Kieso, Jerry J. Weygandt, Terry D. Warfield, Irene M. Wiecek, Bruce J. McConomy