Comprehensive: Power Ltd. has a defined benefit pension plan. At the end of 20X0, the financial statements

Question:

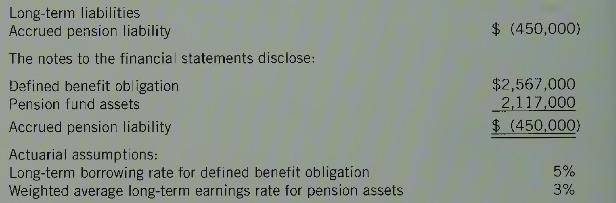

Comprehensive: Power Ltd. has a defined benefit pension plan. At the end of 20X0, the financial statements showed the following:

Assumptions and policies have not changed in 20X1. Actual fund earnings in \(20 \mathrm{X} 1\) were a loss of \(\$ 156,000\). Current service cost was \(\$ 246,000\) in \(20 \times 1\), and benefits paid to pensioners were \(\$ 219,000\). In \(20 X 1\), there was an actuarial review that showed that the corrected value for the opening defined benefit obligation was \(\$ 2,899,000\), not \(\$ 2,567,000\) (a \(\$ 332,000\) increase). The estimate was changed because of longer expected lives of employees. This amount has already vested. In addition, Power granted past service cost benefits to employees with an effect of increasing the accrued benefit obligation by \(\$ 675,000\) (effective 1 January). Amortization of this amount will commence in \(20 \mathrm{Xl}\), over the five-year vesting period. As a result of these two adjustments, the defined benefit obligation was \(\$ 3,574,000(\$ 2,567,000+\$ 332,000+\) \(\$ 675,000\) ) on 1 January 20X1. The average remaining service period and the expected period to full eligibility of the employee group is 18 years. At the end of the year, Power funded current service cost plus \(\$ 40,000\) for partial payment of past service cost, plus another \(\$ 100,000\) in part payment for the change in actuarial liability. Power uses the corridor method for changes in the defined benefit obligation caused by changes in estimates; the 20X1 change was effective 1 January and should be evaluated for amortization in 20X1.

Required:

1. What actuarial cost method would have been used to calculate current service cost? What is/are the major forecasted variable(s) in this actuarial cost model that is/are different than those of the other actuarial cost models?

2. Calculate pension expense for \(20 \mathrm{X} 1\), and the closing balance of the recorded accrued pension liability. Also calculate the closing balance of the defined benefit obligation and the fund assets held by the trustee.

3. Explain how (or if) the economic status (funded status) of the pension plan differs from the recorded pension asset or liability position at the end of 20X0 and then at the end of \(20 \times 1\) if Power used the accounting policies as in requirement 2.

4. Calculate pension expense for \(20 \mathrm{X} 1\), assuming that the company includes all actuarial gains and losses in earnings as they occur.

5. Calculate pension expense, and prepare the pension entry(ies), assuming that the company includes all actuarial gains and losses as a reserve as they occur, with the annual actuarial gains and losses reported as an element of other comprehensive income.

6. Comment on the differences in requirements 2,4 , and 5.

7. Calculate pension expense for \(20 \mathrm{X} 1\) if Power were a private corporation that has elected to use the simplified approach to pension accounting.

8. Calculate pension expense for \(20 \mathrm{X} 1\) if Power were a private company and the pre-2011 Canadian GAAP approach to pension accounting is used. Use the \(10 \%\) corridor rule for actuarial gains and losses.

Step by Step Answer: