Davenport Department Store converted from the conventional retail method to the LIFO retail method on January 1,

Question:

Davenport Department Store converted from the conventional retail method to the LIFO retail method on January 1, 2012, and is now considering converting to the dollar-value LIFO inventory method. During your examination of the financial statements for the year ended December 31, 2013, management requested that you furnish a summary showing certain computations of inventory cost for the past 3 years.

Here is the available information.

1. The inventory at January 1, 2011, had a retail value of $56,000 and cost of $29,800 based on the conventional retail method.

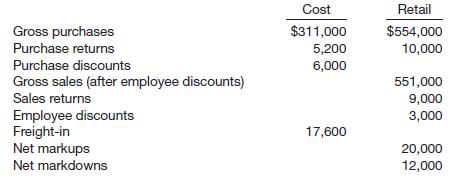

2. Transactions during 2011 were as follows.

3. The retail value of the December 31, 2012, inventory was $75,600, the cost ratio for 2012 under the LIFO retail method was 61%, and the regional price index was 105% of the January 1, 2012, price level.

4. The retail value of the December 31, 2013, inventory was $62,640, the cost ratio for 2013 under the LIFO retail method was 60%, and the regional price index was 108% of the January 1, 2012, price level.

Instructions

(a) Prepare a schedule showing the computation of the cost of inventory on hand at December 31, 2011, based on the conventional retail method.

(b) Prepare a schedule showing the recomputation of the inventory to be reported on December 31, 2011, in accordance with procedures necessary to convert from the conventional retail method to the LIFO retail method beginning January 1, 2012. Assume that the retail value of the December 31, 2011, inventory was $60,000.

(c) Without prejudice to your solution to part (b), assume that you computed the December 31, 2011, inventory (retail value $60,000) under the LIFO retail method at a cost of $33,300. Prepare a schedule showing the computations of the cost of the store’s 2012 and 2013 year-end inventories under the dollar-value LIFO method.

Step by Step Answer: