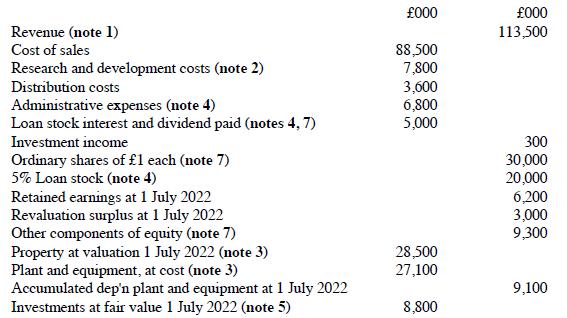

The following trial balance extracts relate to Moston as at 30 June 2023: The following notes are

Question:

The following trial balance extracts relate to Moston as at 30 June 2023:

The following notes are relevant:

1. Revenue includes a £3 million sale (which was made on 1 January 2023) of maturing goods. The carrying amount of these goods at the date of sale was £2 million. Moston is still in possession of the goods (but they have not been included in inventory) and has an option to repurchase them at any time in the next three years. In three years’ time the goods are expected to be worth £5 million. The repurchase price will be the original selling price plus interest at 10% per annum from the date of sale to the date of repurchase.

2. Moston commenced a research and development project on 1 January 2023. It spent £1 million per month on research until 31 March 2023, at which date the project passed into the development stage. From this date it spent £1. 6 million per month until the year end (30 June 2023), when development was completed. However, it was not until 1 May 2023 that the directors of Moston were confident that the new product would be a commercial success. Expensed research and development costs should be charged to cost of sales.

3. Moston’s property is carried at fair value, which at 30 June 2023 was £29 million. The remaining life of the property at the beginning of the year (1 July 2022) was 15 years. The company does not make an annual transfer to retained earnings in respect of the revaluation surplus. Ignore deferred tax on the revaluation. Plant and equipment is depreciated at 15% per annum using the reducing balance method. No depreciation has yet been charged on any non-current asset for the year ended 30 June 2023. All depreciation is charged to cost of sales.

4. The 5% loan stock was issued on 1 July 2022 at its nominal value of £20 million. Direct issue costs of £500,000 have been charged to administrative expenses. The loan stock will be redeemed after three years at a premium which gives an effective finance cost of 8% per annum. Annual interest was paid on 30 June 2023.

5. The investments (holdings of ordinary shares) had a fair value of £9.6 million at 30 June 2023. There were no acquisitions or disposals of investments during the year.

6. A provision of £1.2 million is required for current tax for the year ended 30 June 2023, together with an increase to the deferred tax provision to be charged to profit or loss of £800,000.

7. Moston paid a dividend of 20p per share on 30 March 2023, which was followed by an issue of 10 million ordinary shares at their market value of £1.70 per share. The share premium on the issue was recorded in other components of equity.

Required:

Prepare the following financial statements for Moston:

(a) a statement of comprehensive income for the year to 30 June 2023

(b) a statement of changes in equity for the year to 30 June 2023.

Step by Step Answer:

a Moston Statement of Comprehensive Income Revenue 113500 Cost of sales 88500 Gross profit ...View the full answer

International Financial Reporting a practical guide

ISBN: 9781292439426

8th Edition

Authors: Alan Melville