Prove the following bounds on European call options C(S, t), on an underlying share price S, with

Question:

Prove the following bounds on European call options C(S, t), on an underlying share price S, with no dividends:

(a) CA ≥ CB, where CA and CB are calls with the same exercise price E and expiry dates TA and TB respectively, and TA > TB.

(b)

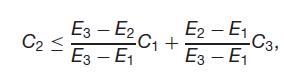

where C1,C2 and C3 are calls with the same expiry T, and have exercise prices E1, E2 and E3 respectively, where E1 < E2 < E3.

Consider E2 = λE1 + (1 − λ)E3.

Fantastic news! We've Found the answer you've been seeking!

Step by Step Answer:

a The value of a call option at expiration is equal to the maximum of 0 or the dif...View the full answer

Answered By

Dulal Roy

As a tutor, I have gained extensive hands-on experience working with students one-on-one and in small group settings. I have developed the ability to effectively assess my students' strengths and weaknesses, and to customize my teaching approach to meet their individual needs.

I am proficient at breaking down complex concepts into simpler, more digestible pieces, and at using a variety of teaching methods (such as visual aids, examples, and interactive exercises) to engage my students and help them understand and retain the material.

I have also gained a lot of experience in providing feedback and guidance to my students, helping them to develop their problem-solving skills and to become more independent learners. Overall, my hands-on experience as a tutor has given me a deep understanding of how to effectively support and encourage students in their learning journey.

0 Reviews

10+ Question Solved

Related Book For

Question Posted: