Refer to the Chapter 4 discussion (Appendix 4, pp. 1409) of the billing department at a customer

Question:

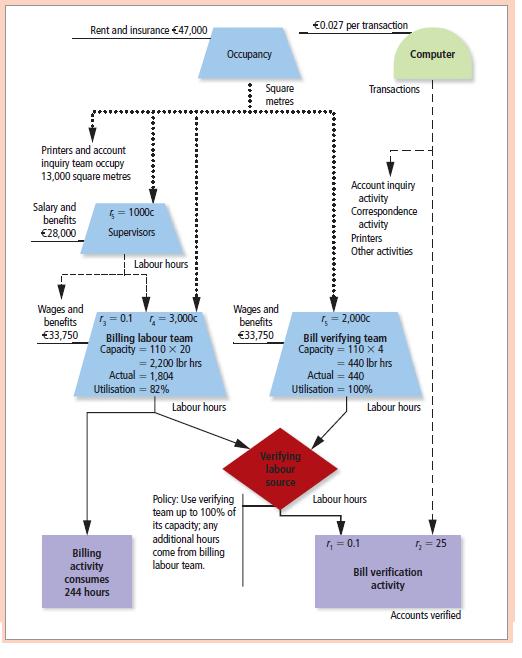

Refer to the Chapter 4 discussion (Appendix 4, pp. 140–9) of the billing department at a customer care centres. Suppose the billing department has designed an MSABC system. Exhibit 12.20 shows the process map for the MSABC system. Consider the portion of the billing department’s process map shown in Exhibit 12.21. Management wants to reduce activities that do not add value for the customer. One idea is to reduce the verification of commercial bills by verifying only 70 per cent of commercial bills (at random) and, further, by verifying only certain parts of each bill. Verifying only part of each bill will reduce the verifying time from 6 minutes to only 3 minutes per bill (account). Management believes that this procedure would not result in any increase in the number of inquiries and that bill accuracy would be unchanged. Since only part of each bill will be verified, the number of computer transactions will also be reduced from 25 to 15 per account. The company’s labour agreement specifies that whenever labour utilization for the combined billing and verification labour pool falls below 70 per cent due to any process improvement, the company may lay off workers until the utilization level reaches 70 per cent.

Currently, billing labour (billing labour plus bill-verifying labour) utilization is at 85 per cent (actual hours consisting of 1,804 labour hours for billing plus 440 labour hours for verification activity

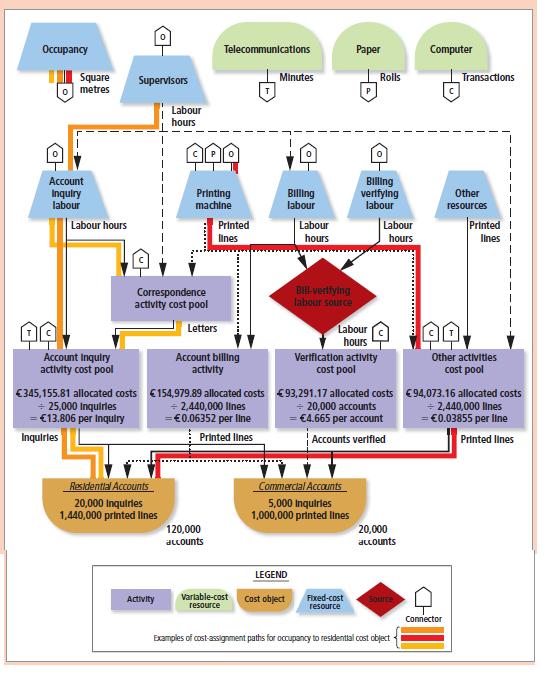

Exhibit 12.20

Exhibit 12.21

divided by capacity of 2,640 labour hours = 85 per cent). Wages and benefits are €2,812.50 per month per laborer. Each laborer is available for 110 hours a month. Currently, there are 24 billing laborers, 4 of whom are dedicated to verifying bills – the verification team. Because of the negative impact that layoffs have on employee morale, management is hesitant to implement any layoffs unless the cost savings are significant. Cost allocation in MSABC systems is complex and requires some form of computer software.

divided by capacity of 2,640 labour hours = 85 per cent). Wages and benefits are €2,812.50 per month per laborer. Each laborer is available for 110 hours a month. Currently, there are 24 billing laborers, 4 of whom are dedicated to verifying bills – the verification team. Because of the negative impact that layoffs have on employee morale, management is hesitant to implement any layoffs unless the cost savings are significant. Cost allocation in MSABC systems is complex and requires some form of computer software.

To get a feel for this complexity, consider the various cost-allocations required to allocate occupancy cost to the residential accounts. Three of these paths are listed below and are also displayed in Exhibit 12.20.

Allocation Path 1: Occupancy → Account Inquiry Labour → Correspondence Activity → Account Inquiry Activity → Residential Accounts Allocation Path 2: Occupancy → Supervision → Account Inquiry Labour → Account Inquiry Activity → Residential Accounts Allocation Path 3: Occupancy → Printers → Other Activities → Residential Accounts A computer program, either a spreadsheet or commercial software, would compute the allocations for each step in these paths based on the percentage of cost-allocation bases used. For example, the first set of allocations of the €47,000 occupancy costs are based on the square meters occupied by account-inquiry labour, supervisors, printing machines, billing labour and bill-verifying labour.

1. There are a total of eleven allocation paths to allocate occupancy costs to residential accounts. Give the other eight paths, using the same format shown previously.

2. In Exhibit 12.21, the relationship (indicated by arrows and consumption rates) between the computer resource and activities and resources such as account inquiry, correspondence, printing machines and other activities is not shown. Explain why it is not necessary to know these relationships in order to determine the incremental billing labour cost savings from the process improvement.

3. Why is ‘transactions’ a true cost driver for computer costs, whereas supervisor ‘labour hours’ is not a true cost driver of billing labour costs?

4. Determine the billing labour and computer cost savings from this process improvement. What other potential cost savings may result? What action would you recommend?

Step by Step Answer:

1 The remaining eight costallocation paths are as follows Allocation Path 4 Occupancy Account Inquiry Activity Account Inquiry Labour Residential Accounts Allocation Path 5 Occupancy Supervision Accou...View the full answer

Introduction To Management Accounting

ISBN: 9780273737551

1st Edition

Authors: Alnoor Bhimani, Charles T. Horngren, Gary L. Sundem, William O. Stratton, Jeff Schatzberg