Professor I.M. Mean likes to use averages. When fitting a regression model (y_{i}=beta_{1}+beta_{2} x_{i}+e_{i}) using the (N=6)

Question:

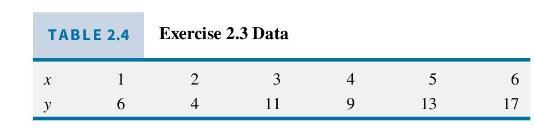

Professor I.M. Mean likes to use averages. When fitting a regression model \(y_{i}=\beta_{1}+\beta_{2} x_{i}+e_{i}\) using the \(N=6\) observations in Table 2.4 from Exercise 2.3, \(\left(y_{i}, x_{i}\right)\), Professor Mean calculates the sample means (averages) of \(\left(y_{i}, x_{i}\right)\) for the first three and second three observations in the data \(\left(\bar{y}_{1}=\sum_{i=1}^{3} y_{i} / 3, \bar{x}_{1}=\sum_{i=1}^{3} x_{i} / 3\right)\) and \(\left(\bar{y}_{2}=\sum_{i=4}^{6} y_{i} / 3, \bar{x}_{2}=\sum_{i=4}^{6} x_{i} / 3\right)\). Then Dr. Mean's estimator of the slope is \(\hat{\beta}_{2, \text { mean }}=\left(\bar{y}_{2}-\bar{y}_{1}\right) /\left(\bar{x}_{2}-\bar{x}_{1}\right)\).

a. Assuming assumptions SR1-SR6 hold, show that, conditional on \(\mathbf{x}=\left(x_{1}, \ldots, x_{6}\right)\), Dr. Mean's estimator is unbiased, \(E\left(\hat{\beta}_{2, \text { mean }} \mid \mathbf{x}\right)=\beta_{2}\).

b. Assuming assumptions SR1-SR6 hold, show that \(E\left(\hat{\beta}_{2, \text { mean }}\right)=\beta_{2}\).

c. Assuming assumptions SR1-SR6 hold, find the theoretical expression for \(\operatorname{var}\left(\hat{\beta}_{2, \text { mean }} \mid \mathbf{x}\right)\). Is this variance larger or smaller than the variance of the least squares estimator \(\operatorname{var}\left(b_{2} \mid \mathbf{x}\right)\) ? Explain.

Data From Table 2.4:-

Step by Step Answer:

Principles Of Econometrics

ISBN: 9781118452271

5th Edition

Authors: R Carter Hill, William E Griffiths, Guay C Lim