When we estimated an error correction model for the bond and federal funds rates in Example 12.9,

Question:

When we estimated an error correction model for the bond and federal funds rates in Example 12.9, we estimated the coefficients of the cointegrating relationship \(B R_{t}=\beta_{1}+\beta_{2} F F R_{t}+e_{t}\) at the same time as we estimated the other coefficients. Return to that example and estimate the error correction model with the cointegrating relationship replaced by the lagged residuals \(\hat{e}_{t-1}=B R_{t-1}-\) \(1.328-0.832 F F R_{t-1}\). Compare your estimates with those obtained in Example 12.9, reported in equation (12.32).

Data From Example 12.9:-

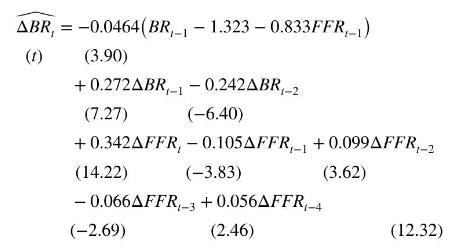

For an error correction model relating changes in the bond rate to the lagged cointegrating relationship and changes in the federal funds rate, it turns out that up to four lags of \(\triangle F F R_{t}\) are relevant and two lags of \(\Delta B R_{t}\) are needed to eliminate serial correlation in the error. The equation estimated directly using nonlinear least squares is

Notice that the estimates \(\hat{\beta}_{1}=1.323\) and \(\hat{\beta}_{2}=0.833\) are very similar to those obtained from direct OLS estimation of the cointegrating relationship in (12.30). The relationship between all the coefficients in (12.32) and its corresponding ARDL model are explored in Exercise 12.18.

If we use the residuals \(\hat{e}_{t}=B R_{t}-1.323-0.833 F F R_{t}\), obtained from the estimates in (12.32), to test for cointegration, we get a similar result to our earlier one

\[\begin{gathered}\widehat{\Delta e_{t}}=-0.0819 \hat{e}_{t-1}+0.224 \Delta \hat{e}_{t-1}-0.177 \Delta \hat{e}_{t-2} \\(\tau \text { and } t)(-5.53)\end{gathered}\]

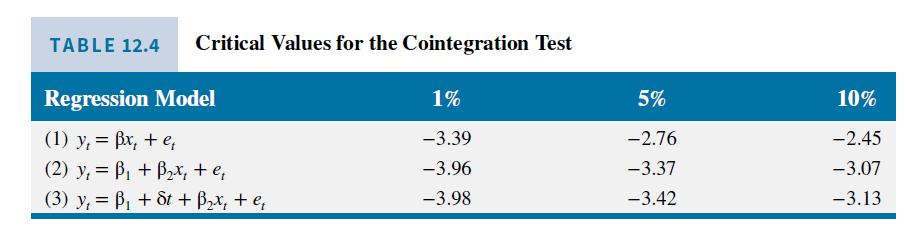

As before, the null hypothesis is that \((B R, F F R)\) are not cointegrated (the residuals are nonstationary). Since the cointegrating relationship includes a constant, the critical value from Table 12.4 is -3.37 . Comparing the actual value \(\tau=-5.53\) with the critical value, we reject the null hypothesis and conclude that \((B R, F F R)\) are cointegrated.

Data From Table 12.4:-

Data From Equation 12.30:-

Step by Step Answer:

Principles Of Econometrics

ISBN: 9781118452271

5th Edition

Authors: R Carter Hill, William E Griffiths, Guay C Lim