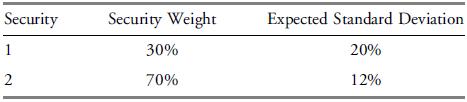

If the standard deviation of the portfolio is 14.40%, the covariance between the two securities is equal

Question:

If the standard deviation of the portfolio is 14.40%, the covariance between the two securities is equal to:

A. 0.0006.

B. 0.0240.

C. 1.0000.

Use the following data to answer Question.

A portfolio manager creates the following portfolio:

Fantastic news! We've Found the answer you've been seeking!

Step by Step Answer:

B is correct A portfolio standard deviation of 1440 is the ...View the full answer

Answered By

HARSH RANJAN

Taken classes at college to graduates, Also worked as an expert to a freelancer online question-solving portal for more than 8 months with an average rating greater than 4.2 out of 5.

1+ Reviews

10+ Question Solved

Related Book For

Investments Principles Of Portfolio And Equity Analysis

ISBN: 9780470915806

1st Edition

Authors: Michael McMillan, Jerald E. Pinto, Wendy L. Pirie, Gerhard Van De Venter, Lawrence E. Kochard

Question Posted: