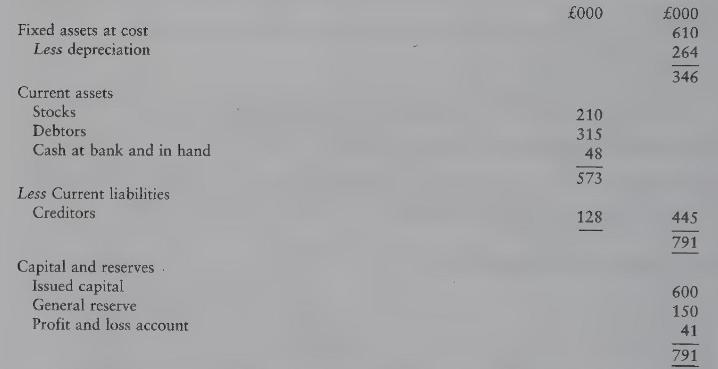

A The summarised balance sheet of Newland Traders at 30 May (19 mathrm{X} 7) was as follows:

Question:

A The summarised balance sheet of Newland Traders at 30 May \(19 \mathrm{X} 7\) was as follows:

Selling and materials prices at 30 May \(19 \times 7\) provide for a gross profit at the rate of 25 per cent of sales.

The creditors at 30 May \(19 \mathrm{X} 7\) represent the purchases for May 19X7, and the debtors the sales for April of \(£ 150,000\) and May of \(£ 165,000\).

Estimates of sales and expenditure for the six months to 30 November \(19 \times 7\) are as follows:

(i) Sales for the period at current prices will be \(£ 800,000\). Sales for the months of September and October will each be twice those of the sales in each of the other months.

(ii) Stock at the end of each month will be the same as at 30 May \(19 \times 7\) except that at 30 November \(19 \mathrm{X} 7\) it will be increased to 20 per cent above that level.

(iii) Creditors will be paid one month after the goods are supplied and debtors will pay two months after the goods are supplied.

(iv) Wages and expenses will be \(£ 20,000\) a month and will be paid in the month in which they are incurred.

(v) Depreciation will be at the rate of \(£ 5,000\) a month.

(vi) There will be capital expenditure of \(£ 80,000\) on 1 September 19X7. Depreciation, in addition to that given in \((v)\) above, will be at the rate of 10 per cent per annum on cost.

(vii) There will be no changes in issued capital, general reserve or prices of sales or purchases.

Required:

(a) Sales and purchases budgets and budgeted trading and profit and loss accounts for the six months ended 30 November \(19 \times 7\).

(b) A budgeted balance sheet as at 30 November \(19 \times 7\).

(c) A cash flow budget for the six months ended 30 November 19X7 indicating whether or not it will be necessary to make arrangements for extra finance and, if so, your recommendation as to what form it should take.

Show all your calculations.

Step by Step Answer: