Winners & Losers, Inc. (WLI) is a Nevada corporation with its principal place of business in Las

Question:

Winners & Losers, Inc. (WLI) is a Nevada corporation with its principal place of business in Las Vegas. Its business model is to provide electronic sports betting in conjunction with a new law that legalized it in Nevada. The company’s shares are registered with the SEC.

It is not against Federal law to gamble on the Internet or place bets on sporting events as an individual. Some states have laws against online gambling, but they are, literally, never enforced. If an individual places bets and does not act as a bookie and accepts wagers, then that party has nothing to worry about from a legal perspective. Moreover, Nevada recently legalized mobile and Internet sports betting throughout the state.

Overview

WLI made improper adjustments to its accrual for bonuses and accounting for stock compensation that enabled it to meet or exceed financial analysts’ earnings projections from the second quarter of 2021 through the fourth quarter of the year. It reported earnings per share (EPS) that did not accurately reflect the company’s underlying performance. During these three consecutive financial quarters, WLI’s then-Corporate Controller, Bonnie Buyers, CPA, directed or otherwise caused her subordinates to book unsupported, manual accounting adjustments to WLI’s management bonus accruals and stock-based compensation. These adjustments did not comply with generally accepted accounting principles (GAAP) and artificially inflated WLI’s income and EPS, which resulted in the company’s meeting or beating consensus estimates for EPS and showing earnings growth. WLI’s then-Chief Financial Officer (CFO), Kathy Sellers, also caused Buyers to direct entries in two quarters that lacked support and did not comply with GAAP. Buyers and Sellers were able to direct or cause the improper adjustments because WLI failed to have sufficient accounting controls or procedures in place to prevent unsupported, manual, period-end, journal entries.

The adjustments were also material to WLI’s financial statements and caused the company to make false disclosures in public filings, press releases, and earnings calls about its actual EPS results, its earnings growth, and its pattern of meeting or beating consensus analyst estimates. Had Buyers (controller) and Sellers (CFO) ensured the financial statements complied with GAAP, WLI’s reported earnings would have been more volatile than reported.

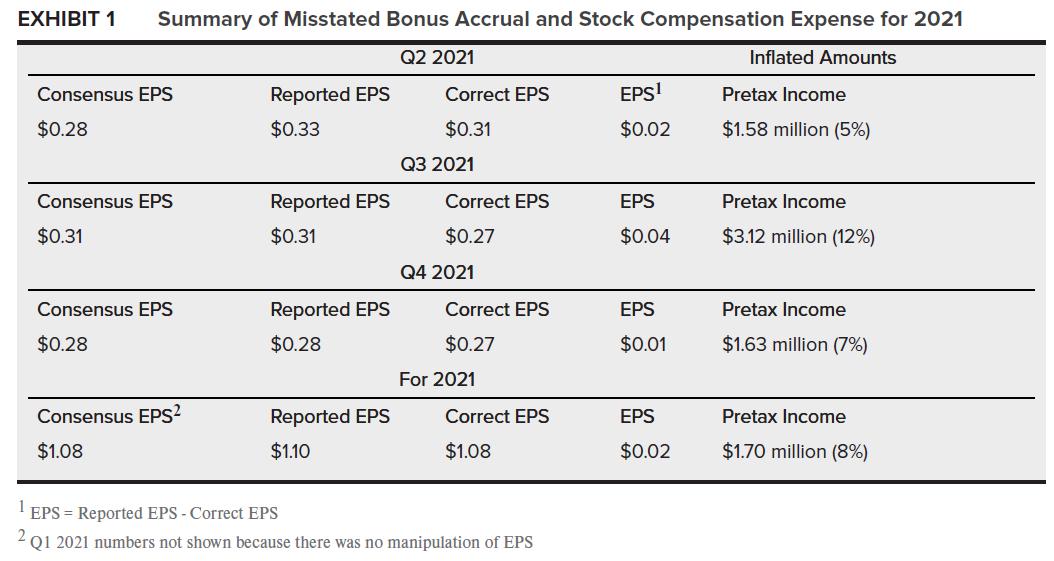

Second Quarter of 2021

In Q2 2021, WLI reported EPS of $0.33 and its earnings release stated that it had “finished with earnings per share that tied our all-time record.” In truth, WLI did not achieve record EPS in Q2 2021 because it understated its actual expenses for management bonuses by $1.58 million, which in turn inflated its pretax income by 5 percent and its EPS by $0.02.

WLI paid nondiscretionary management bonuses based on the achievement of established targets for operating income before incentives (“OIBI”) and cash flow. If WLI met the stated “goal” for those targets, management would receive 100 percent of their bonus potential. If WLI exceeded the goal, management would receive up to a maximum, 150 percent, of their bonus potential depending on the amount by which the goal was exceeded.

At the time that Buyers improperly reduced the bonus accrual, WLI’s best estimate was that annual bonuses at levels greater than 100 percent would be paid. The reduction in the accrual, however, caused WLI’s accrual level to fall far below the 100 percent level, during the closing process for the second quarter, when WLI was on track to report an all-time record EPS of $0.33.

Third Quarter of 2021

In Q3 2021, WLI publicly reported that it had met consensus estimates for EPS of $0.31, reflecting a continued pattern of meeting or beating analyst estimates for two consecutive quarters. In truth, Buyers had directed unsupported accounting entries and otherwise understated expenses, which inflated WLI’s pretax income by 12 percent, or a total of over $3.12 million. Rather than report a meet of consensus EPS estimates, WLI should have reported a $0.04 miss. The improper entries in Q3 2021 concerned WLI’s stock-based compensation and management bonus.

Fourth Quarter of 2021

In Q4 2021, WLI reported a quarterly EPS of $0.28 and an annual EPS of $1.10, which represented a record for WLI and a $0.02 beat of consensus estimates for the year. While the quarter’s EPS was a $0.01 miss of the consensus, it was just enough to allow WLI to report a $0.02 beat of estimates for the year, and the company’s earnings release highlighted that the “fourth quarter rounded out a phenomenal year in which WLI posted all-time records for net income and earnings per share.” In truth, however, WLI’s results were artificially inflated by Buyer’s adjustments to the Consultant’s

bonus and the management bonus.

In total, Buyer’s improper adjustments and Seller’s failure to ensure the bonus accruals were accurate caused Buyers to overstate income by a total of $1.63 million, or 7 percent of the quarter’s pretax income. In reality, WLI should have reported EPS of $0.26 for the quarter and $1.08 for the year, which inflated pretax income by 8 percent for the year, or $1.7 million of pretax income.

Exhibit 1 summarizes the effects of improperly recording the bonus accrual, stock compensation expense, and consultant’s bonus during the three quarters of 2021 and for the year.

WLI Lacked Accurate Books and Records and Sufficient Internal Accounting Controls

These adjustments to WLI’s expenses, which inflated EPS quarter after quarter, were made in part because WLI lacked sufficient internal accounting controls over (a) significant recurring accruals subject to management estimate including incentives and stock-based compensation, (b) journal entries, and (c) period-end adjustments made during the closing process. WLI did not require, for example, corporate-level accounting entries to have supporting documentation, and corporate finance staff regularly recorded manual adjustments with nothing more than an e-mail or oral directive. In addition, Buyer’s direct reports did not analyze or consider the propriety of the entries he directed, and WLI’s Internal Audit function did not perform procedures sufficient to ensure adjustments directed by Sellers and Buyers had support and complied with GAAP.

As a result, WLI’s internal accounting controls were not designed or maintained to provide reasonable assurance that WLI’s financial statements would be presented in conformity with GAAP. WLI’s books, records, and accounts also did not accurately and fairly reflect, in reasonable detail, the company’s transactions.

Questions

1. Do you believe electronic sports betting should be legalized in all states? Use ethical reasoning to support your point of view.

2. Internal accountants and auditors play a critical role in ensuring the financial statements present fairly financial position, net income, and cash flows. Describe the deficiencies in these systems at WLI.

3. Publicly owned companies are not required to have their forward-looking statements audited including earnings guidance, although auditors should make sure statements are not made that conflict with the numbers and other disclosures in the financial statements. Do you believe auditors should be required to audit forward-looking statements and earnings releases? Why or why not?

4. Assume you are a CPA and one of the subordinates who booked unsupported adjustments to bonus accruals, stock compensation expense, and consultant’s bonus for 2021. Explain your ethical obligations under the AICPA Code and the steps you should have taken in lieu of going along with Bonnie Buyer’s directions.

Step by Step Answer:

1 The purpose of this question is to bring students back to the basics and integrate ethical reasoning with discussions in this case study Look for them to address costbenefit analysis in making their ...View the full answer

Ethical Obligations And Decision Making In Accounting Text And Cases

ISBN: 9781264135943

6th Edition

Authors: Steven Mintz