A group has two companies - K ltd, which is operating at just above 50% capacity, and

Question:

A group has two companies -

K ltd, which is operating at just above 50% capacity, and L Ltd, which is operating at full capacity (7000 production hours).

L Ltd produces two products, X andY, using the same labour force for each product. For the next year its budgeted capacity involves a commitment to the sale of 3000 kg of Y. the remainder of its capacity being used on X.

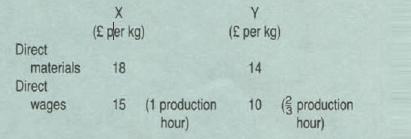

Direct costs of these two products are:

The company's overhead is £126000 per annum relating to X and Yin proportion to their direct wages. At full capacity, £70 000 of this overhead is variable. L ltd prices its products with a 60% mark-up on its total costs.

For the coming year, K Ltd wishes to buy from L Ltd 2000 kg of product X which it proposes to adapt and sell, as product Z, for £100 per kg The direct costs of adaptation are £15 per kg. K Ltd's total fixed costs will not change, but variable overhead of £2 per kg will be incurred.

You are required to recommend, as group management accountant,

(a) at what range of transfer prices. if at all, 2000 kg of product X should be sold to K Ltd; (14 marks)

(b) what other points should be borne in mind when making any recommendations about transfer prices in the above circumstances.

Step by Step Answer: