Aircomposystmes SA has a machining facility specialising in work for the aircraft components market. The prior job-costing

Question:

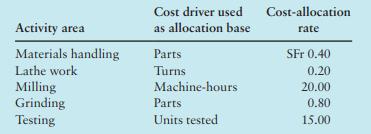

Aircomposystèmes SA has a machining facility specialising in work for the aircraft components market. The prior job-costing system had two direct-cost categories (direct materials and direct manufacturing labour) and a single indirect-cost pool (manufacturing overhead, allocated using direct labour-hours). The indirect-cost-allocation rate of the prior system for the year would have been SFr 115 per direct manufacturing labour-hour. Recently, a team with members from product design, manufacturing and accounting used an activity-based approach to refine its job-costing system. The two direct-cost categories were retained. The team decided to replace the single indirect-cost pool with five indirect-cost pools. These five cost pools represent five activity areas at the facility, each with its own supervisor and budget responsibility. Pertinent data are as follows:

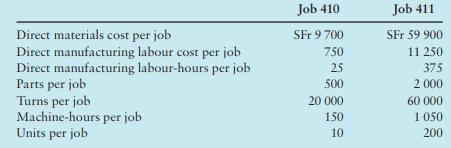

Information-gathering technology has advanced to the point where all the data necessary for budgeting in these five activity areas are automatically collected. Two representative jobs processed under the new system at the facility in the most recent period had the following characteristics:

Required

1. Calculate the per-unit manufacturing costs of each job under the prior job-costing system.

2. Calculate the per-unit manufacturing costs of each job under the activity-based job-costing system.

3. Compare the per-unit cost figures for Jobs 410 and 411 calculated in requirements 1 and 2. Why do the prior and the activity-based costing systems differ in their job cost estimates for each job? Why might these differences be important to Aircomposystèmes?

Step by Step Answer:

Calculation of perunit manufacturing costs of each job under the prior jobcosting system The total manufacturing overhead cost for the prior jobcosting system can be calculated as follows Total Manufa...View the full answer

Management And Cost Accounting

ISBN: 9781292232669

7th Edition

Authors: Alnoor Bhimani, Srikant M. Datar, Charles T. Horngren, Madhav V. Rajan