Intermediate: Key/limiting factor decision-making BVX Limited manufactures three garden furniture products - chairs, benches and tables. The

Question:

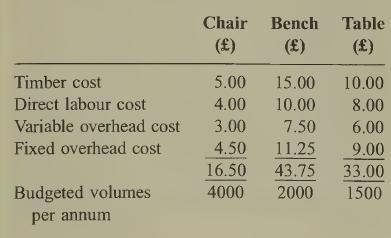

Intermediate: Key/limiting factor decision-making BVX Limited manufactures three garden furniture products - chairs, benches and tables. The budgeted unit cost and resource requirements of each of these items is detailed below:

These volumes are believed to equal the market demand for these products.

The fixed overhead costs are attributed to the three products on the basis of direct labour hours. The labour rate is £4.00 per hour.

The cost of the timber is £2.00 per square metre. The products are made from a specialist timber. A memo from the purchasing manager advises you that because of a problem with the supplier it is to be assumed that this specialist timber is limited in supply to 20 000 square metres per annum.

The sales director has already accepted an order for 500 chairs, 100 benches and 150 tables, which if not supplied would incur a financial penalty of £2000. These quantities are included in the market demand estimates above.

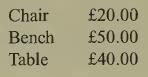

The selling prices of the three products are:

Required:

(a) Determine the optimum production plan and state the net profit that this should yield per annum. (10 marks)

(b) Calculate and explain the maximum prices which should be paid per sq. metre in order to obtain extra supplies of the timber. (5 marks)

(c) The management team has accused the accountant of using too much jargon.

Prepare a statement which explains the following terms in a way that a multi/disci¬ plinary team of managers would understand. The accountant will use this statement as a briefing paper at the next management meet¬ ing. The terms to be explained are:

(i) variable costs;

(ii) relevant costs;

(iii) avoidable costs;

(iv) incremental costs;

(v) opportunity costs.

Step by Step Answer: