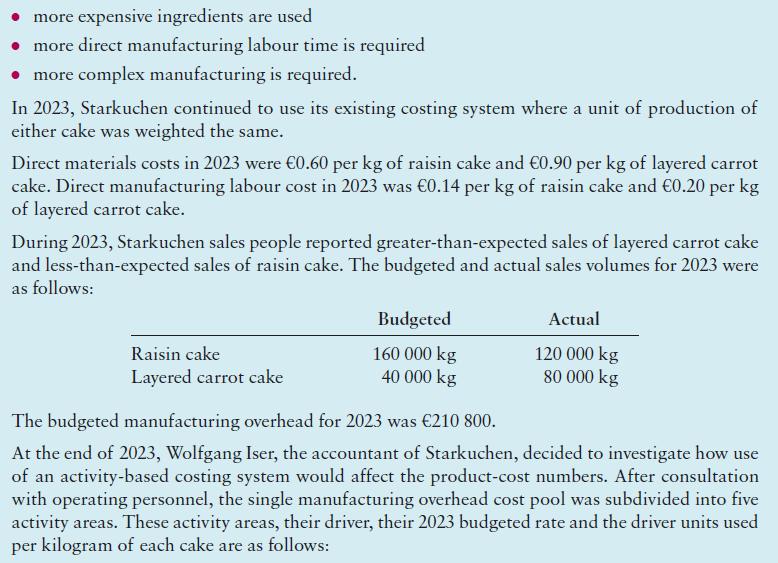

Starkuchen GmbH has been in the food-processing business for three years. For its first two years (2021

Question:

Starkuchen GmbH has been in the food-processing business for three years. For its first two years

(2021 and 2022), its sole product was raisin cake. All cakes were manufactured and packaged in 1 kg units. A normal costing system was used by Starkuchen. The two direct-cost categories were direct materials and direct manufacturing labour. The sole indirect manufacturing cost category –

manufacturing overhead – was allocated to products using a units of production allocation base.

In its third year (2023) Starkuchen added a second product – layered carrot cake – that was packaged in 1 kg units. This product differs from raisin cake in several ways:

Step by Step Answer:

Management And Cost Accounting

ISBN: 9781292436029

8th Edition

Authors: Alnoor Bhimani, Srikant Datar, Charles Horngren, Madhav Rajan