sterbro AS cans peaches for sale to food distributors. All costs are classified as either manufacturing or

Question:

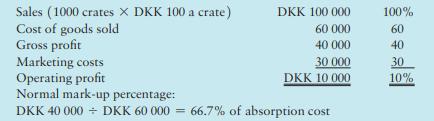

Østerbro AS cans peaches for sale to food distributors. All costs are classified as either manufacturing or marketing. Østerbro prepares monthly budgets. The March 2018 budgeted absorption-costing income statement is as follows:

Monthly costs are classified as fixed or variable (with respect to the cans produced for manufacturing costs and with respect to the cans sold for marketing costs):

Østerbro has the capacity to can 1500 crates per month. The relevant range in which monthly fixed manufacturing costs will be ‘fixed’ is from 500 to 1500 crates per month.

Required

1. Calculate the normal mark-up percentage based on total variable costs.

2. Assume that a new customer approaches Østerbro to buy 200 crates at DKK 55 per crate. The customer does not require additional marketing effort except that additional manufacturing costs of DKK 2000 (for special packaging) will be required. Østerbro believes that this is a one-time-only special order because the customer is discontinuing business in six weeks’ time. Østerbro is reluctant to accept this 200-crate special order because the DKK 55 per crate price is below the DKK 60 per crate absorption cost. Do you agree with this reasoning? Explain.

3. Assume that the new customer decides to remain in business. How would this longevity affect your willingness to accept the DKK 55 per crate offer? Explain.

Step by Step Answer:

Management And Cost Accounting

ISBN: 9781292232669

7th Edition

Authors: Alnoor Bhimani, Srikant M. Datar, Charles T. Horngren, Madhav V. Rajan