Meditech, Inc. manufactures two types of medical devices, Medform and Procel, and applies overhead on the basis

Question:

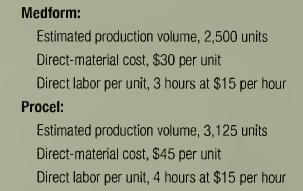

Meditech, Inc. manufactures two types of medical devices, Medform and Procel, and applies overhead on the basis of direct-labor hours. Anticipated overhead and direct-labor time for the upcoming accounting period are \($710,000\) and 20,000 hours, respectively. Information about the company's products follows.

Meditech's overhead of \($710,000\) can be identified with three major activities: order processing (\($120,000),\) machine processing (\($500,000),\) and product inspection (\($90,000).\) These activities are driven by number of orders processed, machine hours worked, and inspection hours, respectively. Data relevant to these activities follow.

Management is very concerned about declining profitability despite a healthy increase in sales volume.

The decrease in income is especially puzzling because the company recently undertook a massive plant renovation during which new, highly automated machinery was installed—machinery that was expected to produce significant operating efficiencies.

Required:

1. Assuming use of direct-labor hours to apply overhead to production, compute the unit manufacturing costs of the Medform and Procel products if the expected manufacturing volume is attained.

2. Assuming use of activity-based costing, compute the unit manufacturing costs of the Medform and Procel products if the expected manufacturing volume is attained.

3. Meditech's selling prices are based heavily on cost.

a. By using direct-labor hours as an application base, which product is overcosted and which product is undercosted? Calculate the amount of the cost distortion for each product.

b. Is it possible that overcosting and undercosting (i.e., cost distortion) and the subsequent determination of selling prices are contributing to the company's profit woes? Explain.

Step by Step Answer:

Managerial Accounting Creating Value In A Dynamic Business Environment

ISBN: 9780071113144

6th Edition

Authors: Ronald W Hilton