Charlesworth plc is a distributor of tiles to the building trade. The vast majority of these tiles

Question:

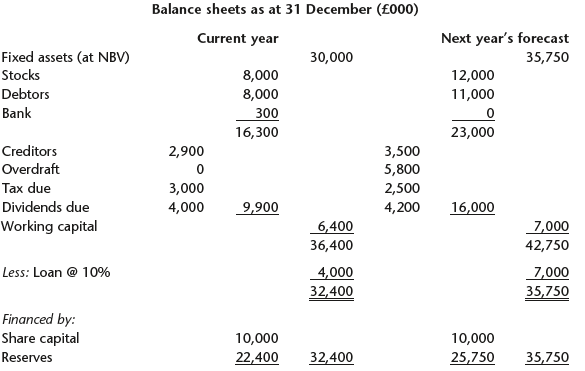

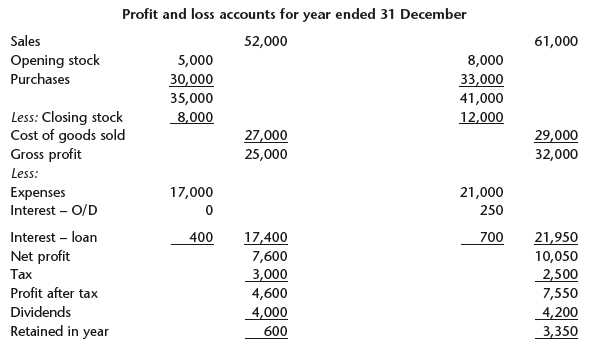

Tasks:

1. Create a cash fl ow statement for next year explaining why the cash position deteriorates during that year.

2. Comment on the company€™s management of working capital by examining the operating and cash cycles for both years and suggest ways in which the company might improve its working capital position.

3. In what other ways could Charlesworth achieve its planned expansion while not breaching the overdraft limit of £1 million?

Fantastic news! We've Found the answer you've been seeking!

Step by Step Answer:

1 Cash flow statement forecast for next year 000 PBIT 11000 10050 700 250 Add back depreciation 5000 Interest paid 950 Stock increase 4000 Debtor incr...View the full answer

Answered By

PALASH JHANWAR

I am a Chartered Accountant with AIR 45 in CA - IPCC. I am a Merit Holder ( B.Com ). The following is my educational details.

PLEASE ACCESS MY RESUME FROM THE FOLLOWING LINK: https://drive.google.com/file/d/1hYR1uch-ff6MRC_cDB07K6VqY9kQ3SFL/view?usp=sharing

3+ Reviews

10+ Question Solved

Related Book For

Managerial Accounting Decision Making and Performance Management

ISBN: 978-0273764489

4th edition

Authors: Ray Proctor

Question Posted: