Refer to the information for Dransfield Company in Exercise 13-31. Required 1. Calculate the amount and cost

Question:

Refer to the information for Dransfield Company in Exercise 13-31.

Required

1. Calculate the amount and cost of unused capacity for:

a. Manufacturing

b. Sales and customer service

c. Advertising

If you are unable to calculate the amount and cost of unused capacity, explain why.

2. State two reasons Dransfield might downsize and two reasons they might not downsize.

3. Assume Dransfield has several product lines, of which ZP98 is only one. The manager for the ZP98 product line is evaluated on the basis of manufacturing and customer sales and service costs, but not advertising costs. The manager wants to increase capacity for customers because he thinks the market is growing, and this will cost an additional $1,098. However, the manager is not going to use this extra capacity immediately, so he classifies it as advertising cost rather than customer sales and service cost. How will the deliberate misclassification of this cost affect:

a. The operating income overall?

b. The growth, price-recovery, and productivity components?

c. The evaluation of the ZP98 manager?

You are not required to calculate any numbers when answering requirement 3. Only discuss whether it will have a positive, negative, or no effect; and comment on the ethics of the manager’s actions.

Data From Exercise 13-31:

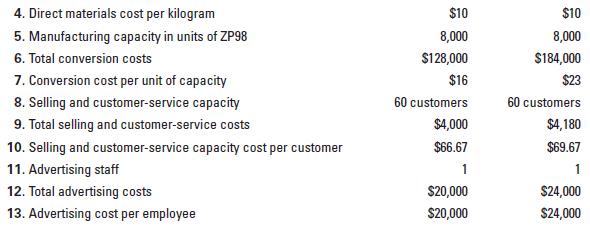

Refer to Exercise 13-30. Assume that in 2016, Dransfield has changed its processes and trained workers to recognize quality problems and fix them before products are finished and shipped to customers. Quality is now at an acceptable level. Cost per kilogram of materials is about the same as before, but conversion costs are higher, and Dransfield has raised its selling price in line with the market. Sales have increased and returns have decreased. Dransfield's managers attribute this to higher quality and a price that is still less than Yorunt's. Information about the current period (2016) and last period (2015) follows.

Conversion costs in each year depend on production capacity defined in terms of ZP98 units that can be produced, not the actual units produced. Selling and customer-service costs depend on the number of customers that Dransfield can support, not the actual number of customers it serves. Dransfield has 50 customers in 2015 and 60 customers in 2016. At the start of each year, management uses its discretion to determine the number of advertising staff for the year. Advertising staff and its costs have no direct relationship with the quantity of ZP98 units produced and sold or the number of customers who buy ZP98.

Data From Exercise 13-30:

Dransfield Company manufactures an electronic component, ZP98. This component is significantly less expensive than similar products sold by Dransfield's competitors. Order-processing time is very short; however, approximately 10% of products are defective and returned by the customer. Returns and refunds are handled promptly. Yorunt Manufacturing, Dransfield's main competitor, has a higher priced product with almost no defects, but a longer order-processing time.

Step by Step Answer:

Calculating the amount and cost of unused capacity a Manufacturing To calculate the amount of unused capacity for manufacturing we need to compare the manufacturing capacity with the actual units prod...View the full answer

Cost Accounting A Managerial Emphasis

ISBN: 978-0133138443

7th Canadian Edition

Authors: Srikant M. Datar, Madhav V. Rajan, Charles T. Horngren, Louis Beaubien, Chris Graham