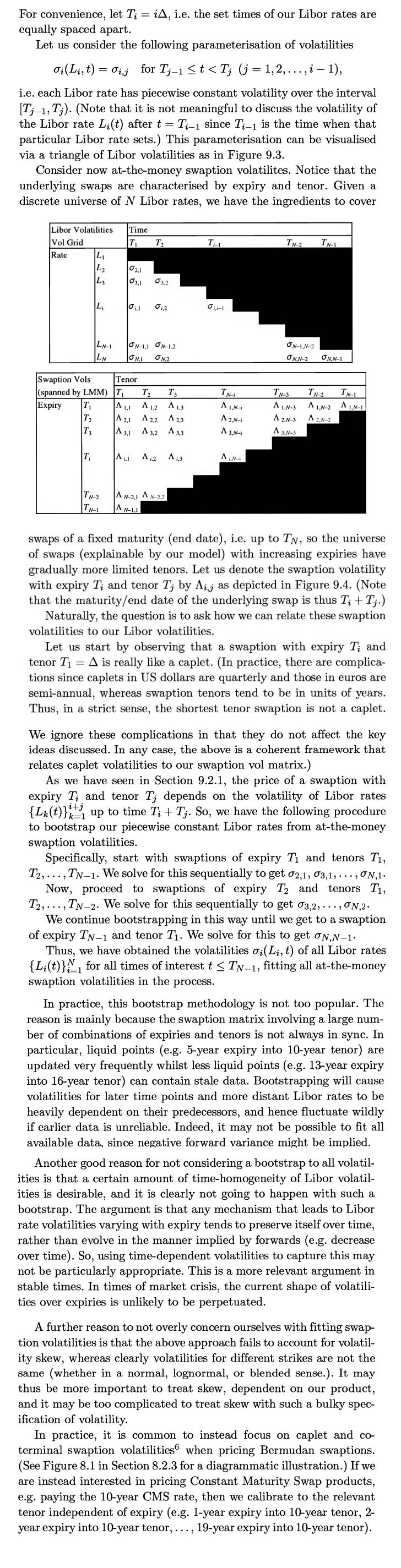

Consider a lognormal Libor Market Model. For simplicity, assume that Libor rates apply over 1y periods. Take

Question:

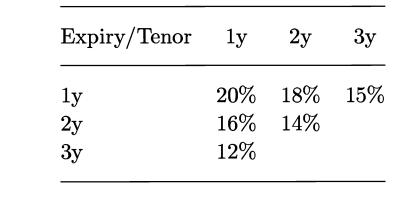

Consider a lognormal Libor Market Model. For simplicity, assume that Libor rates apply over 1y periods. Take current Libor rates to be flat at 3%. Using the discussion on the volatility triangle in Section 9.2.2 and the swaption approximation in Section 9.2.3, obtain the forward vol structure given the following grid of lognormal swaption vols.

Section 9.2.2

Section 9.2.3

Fantastic news! We've Found the answer you've been seeking!

Step by Step Answer:

Answered By

Madhvendra Pandey

Hi! I am Madhvendra, and I am your new friend ready to help you in the field of business, accounting, and finance. I am a College graduate in B.Com, and currently pursuing a Chartered Accountancy course (i.e equivalent to CPA in the USA). I have around 3 years of experience in the field of Financial Accounts, finance and, business studies, thereby looking forward to sharing those experiences in such a way that finds suitable solutions to your query.

Thus, please feel free to contact me regarding the same.

1+ Reviews

10+ Question Solved

Related Book For

Question Posted: