Denoting the FRA rate F(t; Ti1, Ti) as Fi(t), use question 1 to demonstrate that Fi(t) is

Question:

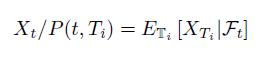

Denoting the FRA rate F(t; Ti−1, Ti) as Fi(t), use question 1 to demonstrate that Fi(t) is a martingale in the Ti forward measure, defined by:

Using the expression for the price of a bond expiring at Tj in terms of one expiring at Ti and the intervening forward rates Fk for i

Fantastic news! We've Found the answer you've been seeking!

Step by Step Answer:

Answered By

Akash Goel

I am in the teaching field since 2008 when i was enrolled myself in chartered accountants course

Since then i have an experience of teaching of class XI, XII, BCOM, MCOM, MBA, CA CPT.

1+ Reviews

10+ Question Solved

Related Book For

The Value Of Uncertainty Dealing With Risk In The Equity Derivatives Market

ISBN: 9781848167728,9781908979582

1st Edition

Authors: George Kaye

Question Posted: